Nautilus NYSE: NLS shares are set to open more than 11% higher after its Q2 earnings release blew away expectations. The home fitness equipment maker reported $114.2 million in revenue, up 94% yoy.

When Nautilus released its Q1 2020 numbers, it raised its Q2 revenue guidance to $94 million. Even that number was well above consensus estimates of a little under $70 million. So the $114.2 million in actual revenue is impressive by any metric.

However, NLS did report a net loss of 17 cents per diluted share. While that was a major improvement over a loss of $2.66 per diluted share in the year-ago quarter, it fell short of consensus estimates for a loss of 10 cents a share.

But the market is paying more attention to the revenue beat than the earnings miss – and for good reason. With Nautilus growing quickly and trading at just over 1x projected full-year 2020 sales, it wouldn’t take super-high margins for the company to become an excellent value in the long run.

Workout-At-Home

Investors from here to Timbuktu have been trying to invest in work-at-home technology. While that’s been a winning play since the onset of the pandemic, it’s far from the only sector that has outperformed over the past few months.

With chains like Planet Fitness forced to close, and faced with onerous social distancing requirements for the foreseeable future, people have decided to set up home gyms to stay in shape.

On its Q1 earnings call, Nautilus noted that demand accelerated over the last few weeks of March, leading revenue to total $93.7 million in Q1 2020, up 11% yoy. That trend continued – benefiting Nautilus for the full Q2.

Operations Became More Efficient in Q2

While earnings came in below expectations, Nautilus’ operating expenses decreased in Q2.

In its press release, NLS noted:

“Adjusted operating expenses decreased by 17.6% to $25.5 million compared to $30.9 million last year, primarily due to continued expense discipline and lower advertising expenses. Customer acquisition costs were meaningfully lower this year as the company pulled back on paid advertising, given strong organic demand and inventory scarcity.”

The Future is Uncertain… But Looks Bright

Nautilus declined to provide guidance for the remainder of 2020, alluding to the “highly volatile environment.”

Of course, all things being equal, if gyms across the country are able to fully re-open, NLS would see lower sales.

With that said, the pandemic doesn’t seem like it will end any time soon. And chances are, most people won’t work out in crowded gyms for several months, if not more.

Furthermore, the longer the pandemic goes on, the more people will buy home fitness equipment. And once the pandemic does end, it’s not as if all of those people are going to put that equipment into storage and return to their pre-COVID workout routines. A large percentage of them will likely continue to work out at home after the pandemic ends – and continue to invest in equipment.

When Will Earnings Materialize?

The price-to-sales ratio is all well and good, but this is the million-dollar question.

NLS is projected to see small losses in 2020 and 2021.

Projections beyond 2021 are inherently uncertain – even moreso due to the emerging trends in the home fitness equipment industry.

That said, Nautilus’ Q2 operational improvements bode well for the future. And even if the company were to achieve a modest 5% net margin in the long run, that would equate to a P/E ratio of around 20 at the current sales and share prices. Add in (likely) revenue growth, and you can see how shares would have a lot of room to run in this scenario.

There’s definitely a level of risk with Nautilus shares – but I think the risk is certainly worth the reward.

Where Can You Get In?

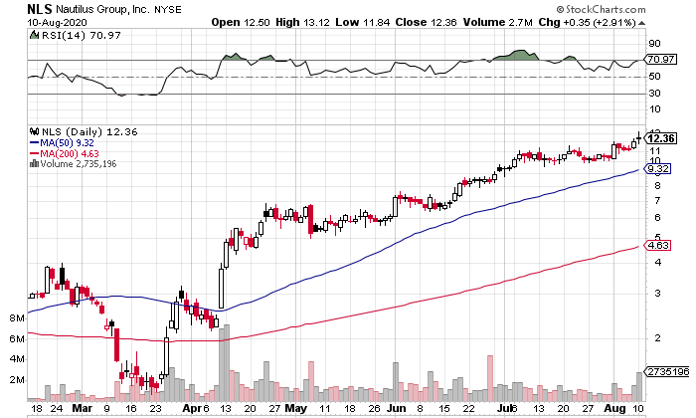

Nautilus shares were extended before the Q2 earnings release, 10xing off the mid-March lows. The RSI just crossed into overbought territory, so shares were also a bit extended from a short-term perspective.

So NLS is going to look very extended following today’s open.

You have two possible entry points:

- Look to get in on the open today, comforted by the long-term upside of NLS.

- Wait for a 2-4 week consolidation with tight price action and low volume, culminating in a decisive breakout.

Either way, if you want to limit your downside, you’re going to have to put your stop-order in a somewhat arbitrary place.

The other option would be to invest for the long run and expose yourself to a higher downside. If you do this, I advise investing a small amount into NLS due to its risky profile.

The Final Word

NLS is one of the biggest pandemic winners in the market – albeit one with a small market-cap. While a lot of its improved outlook is already priced into the shares, NLS still has plenty of upside from here. You should consider getting in now or waiting for a more attractive entry point in the near future.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

MarketBeat's analysts have just released their top five short plays for April 2025. Learn which stocks have the most short interest and how to trade them. Enter your email address to see which companies made the list.

Get This Free Report