Online retailer

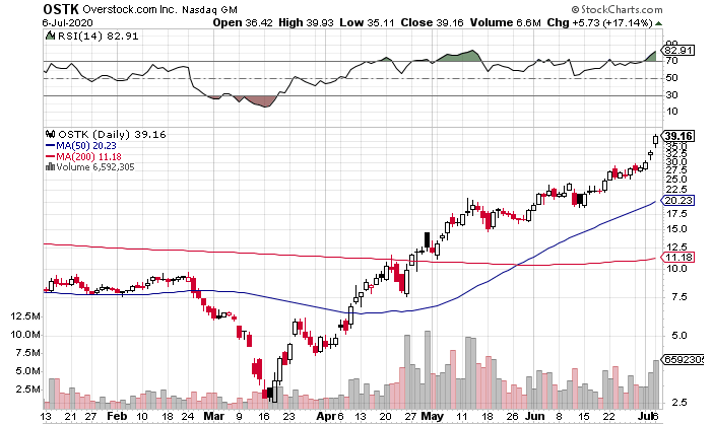

Overstock.com NASDAQ: OSTK has had quite the ride in 2020. After spending the first seven weeks of the year range-bound between around $7.50 and $9.50 a share, pandemic-related fears sent shares down to a mid-March low of $2.53 a share.

Since then, the stock has skyrocketed to nearly $40 a share. That includes yesterday’s gain of around 17%.

So how has Overstock managed to 15x off the lows and quadruple from pre-pandemic levels? And is there still more meat on the bone for investors?

A Perfect Storm

When investors first realized that the pandemic would be a drag on the economy, Overstock was sold off with the rest of the market. After all, it’s hard to hold shares of a company that is losing money when a recession is looming.

But once investors had a chance to evaluate the impact of the pandemic and the numbers started coming in, it became clear that Overstock would thrive in the “new-normal” environment. Let’s start by looking at the retailer’s core operations.

Online Retail

The aptly named Overstock.com largely sells excess inventory from factories and other retailers at discount prices.

Home goods make up the majority of OSTK’s business. With people increasingly shopping online and working from home, demand has surged in this segment. Here are some of the highlights:

- Home goods now make up 87% of sales.

- April sales are up 120% yoy.

- April new customer growth is up 250% yoy.

- Customers have shifted from brick-and-mortar to online, with online increasing from 23% to 42% since the pandemic started.

A bit more on that last point:

This 19% increase represents a monumental shift compared to pre-pandemic trends. There had been a shift prior to the pandemic, but it was happening at around 2% annually over the past 10 years. Overstock leadership acknowledges that this number won’t stay quite that high when the pandemic is fully behind us, but some of the change in habits will stick. Even if the increase is cut in half, from 19% to 9.5%, it would still be a boon for business.

While Overstock’s online retail business is thriving, the company has an additional upside from an unexpected industry.

Blockchain

Overstock has become a player in blockchain, led by tZERO, its alternative trading system (ATS).

OSTK has done an excellent job of growing tZERO; as of May, the platform accounts for 95% of all security-token volume. May saw 423,000 transactions, up over 4x yoy. The tZERO crypto app user base saw 15% growth over the prior month.

The catalyst for this recent move was Overstock’s issuing of a digital preferred stock dividend in May, which traded exclusively on the tZERO platform. Shareholders received one security token for every 10 OSTK shares.

CEO Jonathan E. Johnson III had this to say on the digital dividend during the Q1 2020 earnings call

“This dividend is not a cryptocurrency. It's a preferred share of stock…. these Series A shares are preferred shares and pay a cash dividend and have each of the three years since issuance. Third, distribution of the Series A OSTKO shares to all record date shareholders should increase participation on the tZERO platform, as investors seek to buy and sell shares and broker-dealers seek to execute trades on behalf of their clients.”

While tZERO accounted for just 3% of Q1 2020 revenue, some believe that Overstock’s blockchain business has huge upside. In a recent review, DA Davidson analyst Tom Forte valued Overstock’s blockchain family of businesses at up to $21 per share. There are clearly a lot of assumptions to get to that number, but even if tZERO doesn’t take off, Overstock shares represent a solid value.

Valuation

Overstock is trading at a TTM price-to-sales ratio of less than 1x, which looks great at first glance.

As touched on earlier though, the company is still losing money. But investors shouldn’t be too concerned, as Overstock has the potential for huge growth. Its industry is a $300 billion market when both brick-and-mortar and e-commerce are factored in. The massive recent shift to e-commerce plus the underlying strength of OSTK’s business makes it well-positioned to grab a bigger chunk of market share.

Furthermore, the gross profit margin is trending in the right direction; it was 21.9% in Q1, up 200 basis points yoy. Adjusted EBITDA also increased yoy; while still a loss, it was just $1.9 million in the red.

Bottom line, even after the massive run-up, Overstock is still an excellent risk/reward at these levels. But finding a good entry point is a bit of a challenge.

Technicals

Overstock has basically gone straight up since mid-March. It has never consolidated for more than a couple of weeks on its way up. Shares are up more than 33% in just the past five trading sessions. The RSI is now well into overbought territory.

So where does that leave you?

I wouldn’t initiate a big position right now. Instead, I would look for either:

- A tight consolidation for at least a few weeks that culminates in a high-volume breakout.

- A pullback to the 50-day moving average. This scenario could take quite a while, as the 50-day currently sits at just over half of Overstock’s share price, but it could give you a nice entry point in the next couple of months.

All that said, there’s a good argument to bite the bullet and get into Overstock now. If you want to do that, I would advise initiating a small position that you can add to later on if the chart shapes up.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

If a company's CEO, COO, and CFO were all selling shares of their stock, would you want to know? MarketBeat just compiled its list of the twelve stocks that corporate insiders are abandoning. Complete the form below to see which companies made the list.

Get This Free Report