Enterprise mail and e-commerce solutions provider

Pitney Bowes (NYSE: PBI) stock recently spiked on the $6.6 billion acquisition of peer

Stamps.com NASDAQ: STMP by private equity firm Thomas Bravo. Shares spiked 15% in sympathy before peaking and falling back down. The surprise acquisition brings Pitney Bowes into the spotlight as a potential acquisition target down the road as well as raises its valuation based on the $330-per share purchase price. Pitney Bowes is not the most exciting company as is any company that deals in mail and

documents. However, it is steady, stable and should trade at a higher valuation thanks to the Stamps.com acquisition which placed a nearly 30% premium on shares. It’s a turnaround and valuation narrative, thanks to its digital transformation and

e-commerce pipeline. It’s also one of the largest publicly traded competitors to the U.S. post office and Stamps.com. In fact, the Company did 6X the revenues of Stamps.com, but trades at a much lower valuation. Prudent value investors can watch shares of Pitney Bowes for opportunistic pullback entries to gain exposure.

Q1 FY 2021 Earnings Release

On April 30, 2021, Pitney Bowes released its fiscal first-quarter 2021 results for the quarter ending March 2021. The Company reported an earnings-per-share (EPS) profit of $0.07 excluding non-recurring items versus consensus analyst estimates for a profit of $0.05, a $0.02 beat. GAAP earnings were (-$0.18) which includes a loss related to debt financing. Adjusted EPS includes a $0.02 tax benefit from affiliate reorganization. Revenues grew 14.9% year-over-year (YoY) to $915.2 million beating analyst estimates for $873.82 million. The Company reduced debt by $126 million from year-end 2020. Global Ecommerce revenues rose 41% YoY. Pitney Bowes CEO Mark Lautenbach stated, “We delivered a solid start to the year, with every business making a meaningful contribution to our first-quarter results. Revenue continued to demonstrate strong growth, every business improved its EBIT performance from prior year, and we strengthened our balance sheet. As we enter the final chapter of our transformation, we are well-positioned to reach our ultimate goal of achieving improved profitable revenue growth.”

Full-Year 2021 Guidance

Pitney Bowes expects to grow full-year 2021 annual revenues in the low-to-mid single digits. Adjusted EPS is expected to grow over the prior year driven by improvement in Global Ecommerce. However, the Company expects lower free cash flow due to one-time benefits in 2020, not expected in 2021.

Conference Call Takeaway

CEO Lautenbach set the tone, “For the second consecutive quarter, SendTech improved EBIT on a year-to-year basis. As I mentioned before, the transformation of SendTech from a business in secular decline to a business well-positioned to capture new value in the shipping market is one of the most impressive transformations I’ve ever seen. The businesses has leveraged digital technologies to transform our offerings and our go-to-market strategy. SendTech’s platform is built on IoT technologies that are delivered on a fast chassis and this business is very well-positioned going forward.” He also detailed the Presort business continued momentum in 2020. Global Ecommerce is the growth driver with 40% YoY growth and a nearly 400 basis point improvement in EBIT margins. However, transportation costs has remained high for both E-commerce and Presort but plans to fix that with automation solutions and insource transportation. He concluded, “ It’s hard to call the first quarter an inflection point given the nominal EBIT increase, but revenue and profit did increase and are very much like our position going forward. Each business is poised to continue to make progress during this year and for that matter, going forward beyond this year. All in all, I’m quite pleased with the quarter. It turned in another strong revenue performance and improved EBIT across each segment compared to the prior year.”

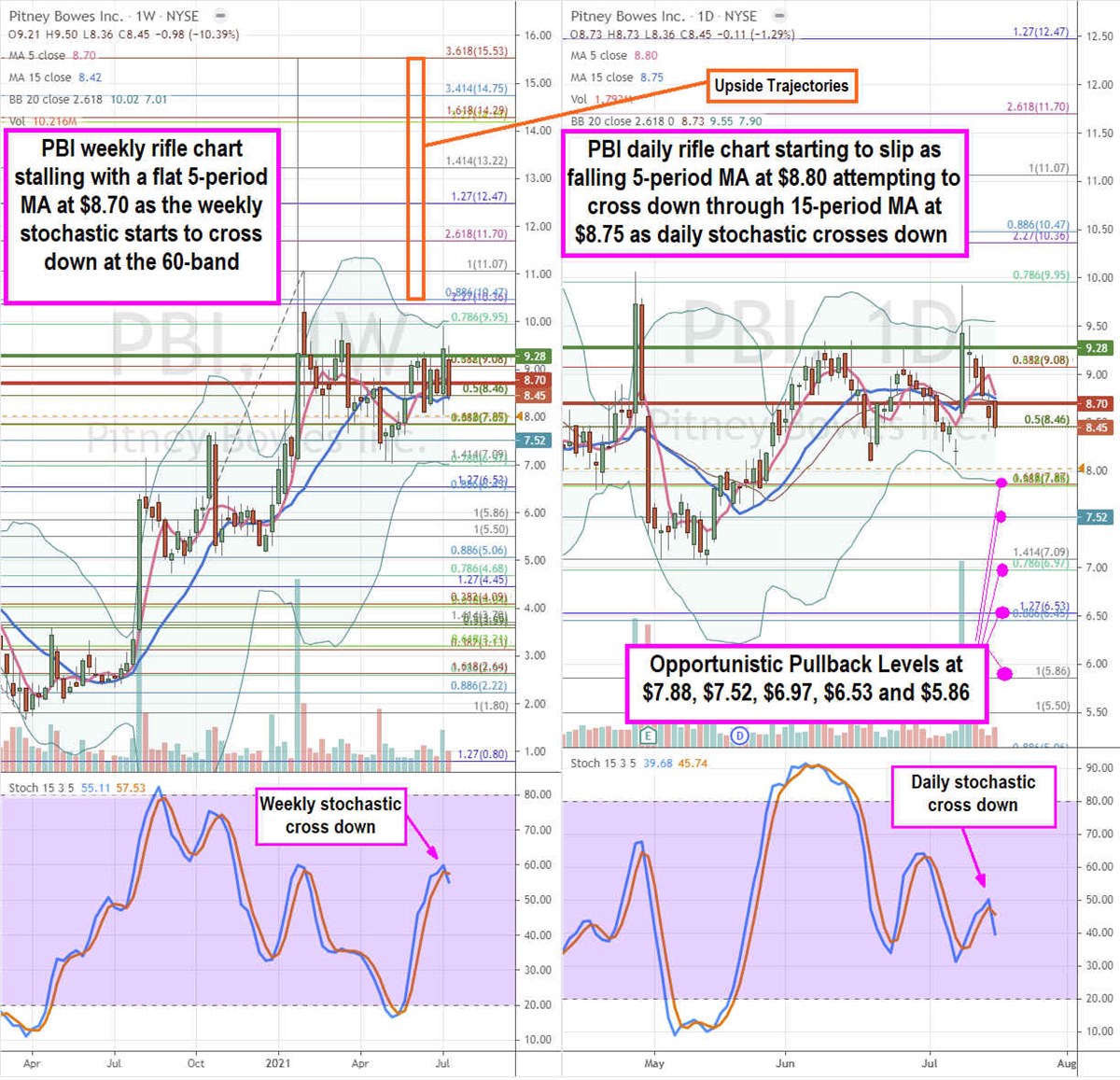

PBI Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provides a precision view of the playing field for PBI shares. The weekly rifle chart peaked off $15.53 Fibonacci (fib) level. The weekly 5-period moving average (MA) went flat at $8.70 with the 15-period MA at the $8.42 fib. The weekly stochastic is crossing down indicating the momentum is failing. The weekly form a market structure high (MSH) sell triggered under $8.70. The weekly market structure low (MSL) buy triggers on the breakout through $9.28. The daily rifle chart is also starting to peak out as the 5-period MA is falling at $8.80 for a potential crossover breakdown through the 15-period MA at $8.75. The daily stochastic failed the mini pup attempt and crossed back down as the divergence top resumes with lower Bollinger Bands (BBs) at $7.88. Prudent investors can monitor for opportunistic pullback levels at the $7.88 daily lower BBs/fib, $7.52 stinky 2.50s, $6.97 fib, $6.53 fib, and the $5.86 fib. The upside trajectories range from the $10.47 fib up towards the $15.53 fib level.

Before you consider Pitney Bowes, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Pitney Bowes wasn't on the list.

While Pitney Bowes currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Which stocks are hedge funds and endowments buying in today's market? Enter your email address and we'll send you MarketBeat's list of thirteen stocks that institutional investors are buying now.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.