RH (Restoration Hardware) NYSE: RH is set to open up more than 14% today after its Q2 earnings beat expectations, taking shares to all-time highs. The luxury furniture retailer has fared well since the onset of the pandemic. But post-COVID, RH has even more upside.

Q2 Looks Great When You Consider the Context

Restoration Hardware recorded $709.7 million in revenue in Q2, beating expectations of $700.9 million, but increasing just 0.5% yoy.

That growth is better than it looks at first glance for two reasons:

- The company’s revenue came in at $482.9 million in Q1, down 19.3% yoy and falling short of expectations for $490 million. So RH has quickly turned it around.

- Restoration Hardware noted that “business trends have continued to build month over month.” RH Core Demand, which excludes its children, hospitality, and outlets divisions, increased 7% yoy in May. But it recorded a 32% yoy gain in June, 24% in July, 47% in August, and 44% in September (month-to-date).

And earnings were even better due to soaring margins.

EPS came in at $4.90 per share, blowing away expectations of $3.41.

Adjusted gross margins increased 550 basis points yoy to 47.5%, while adjusted operating margin jumped 690 basis points to 21.8%.

As a result, free cash flow doubled to $218 million.

A Good Quarter… But an Even Better Outlook

Roughly flat revenue growth is just about the only bone you could pick with Restoration Hardware’s Q2 report. But revenue growth should accelerate going forward.

No, RH isn’t going to turn into Wayfair NYSE: W with its 80%+ revenue growth. But RH is trading at around 31x forward earnings, while Wayfair is just starting to turn a profit.

And RH can realistically attain low-double-digit revenue growth post-pandemic.

Here are three reasons why:

- Brick-and-mortar revenue decreases will reverse.

In Q2, demand was hurt by a 23% “reduction in open store days” at the company’s furniture galleries. Most stores have now re-opened, but social distancing requirements and a hesitancy to shop at brick-and-mortar locations will be headwinds for the foreseeable future. According to William Blair analyst Daniel Hofkin, digital platforms accounted for just 40% of RH’s sales last year, so this company relies heavily on its physical locations. The business will improve post-pandemic.

- RH’s pivot came at the wrong time but has potential post-COVID.

Pre-COVID, RH was planning to offer hotel rooms for rent, homes for sale, and yachts. The idea was to stock the rooms, homes, and yachts with Restoration Hardware furniture, taking an innovative approach to marketing. There is long-term potential here, as it beats strolling around a sales floor, but it is tough to implement for the time being. Post-COVID, though, this concept has potential.

- The move to the suburbs will benefit RH.

It’s well-established that a sizeable number of people are moving from cities to suburbs as the pandemic has made it clear that most people can carry out their work duties remotely. RH will be a big beneficiary of this trend, but it will take time to play out “as the cycle for purchasing and furnishing a home is anything but quick,” according to CEO Gary Friedman.

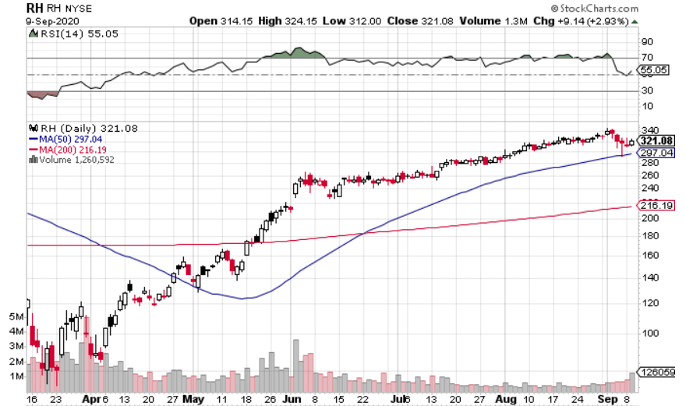

Look for a Bullish Flag Pattern

Expectations were likely sky-high for RH heading into its Q2 earnings, as the company received several recent upgrades. Furthermore, shares were already trading 25% higher than pre-pandemic highs and more than quadruple March 2020 lows.

But the 14%+ increase is well-deserved for RH; the company’s impressive margins and post-COVID revenue growth outlook give shares plenty of upside from here.

That said, shares are extended and you should look for a bullish flag pattern before considering a purchase.

A bullish flag pattern would mean that after today’s move, shares would consolidate for a couple of weeks, followed by a convincing breakout.

The Final Word

Even after exceeding its pre-pandemic highs and more than quadrupling off its March lows, Restoration Hardware shares still have a lot of room to run.

The current valuation is very reasonable when you consider:

- The company’s ability to maintain its revenue in a less-than-ideal environment.

- Soaring margins.

- The three tailwinds that will benefit RH post-COVID.

Look to get in if the bullish flag pattern materializes.

Before you consider RH, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and RH wasn't on the list.

While RH currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Thinking about investing in Meta, Roblox, or Unity? Enter your email to learn what streetwise investors need to know about the metaverse and public markets before making an investment.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.