LCI Industries Has Your Ticket To Ride Out 2020

It is no joke to say that trends within the RV industry are strong. The RV Industry Association reports sales of RVs are up more than 30% on a YOY basis and that is seen in all the earnings results. A month ago, Thor Industries (NYSE:THO) blew past consensus and provided an upgrade to guidance. That strength was echoed by Camping World (NYSE:CWH) and LCI Industries (NYSE:LCII) over the past two days and, in all three cases, demand is strong and expected to stick. If you are looking for a comfortable dividend to ride out 2021 one of these three would be a good choice. But there's a catch, LCI Industries pays the highest yield and has the most growth in its forecast.

"Between the growing trend to work and learn from your RV and the incredible fall and winter RV travel options, we do not see the demand for RVs going down anytime soon. For the year, shipments stand at 300,100 units, off just 3.2% (YOY) as the RV industry continues to overcome the nearly two-month shutdown this Spring due to the Covid-19 pandemic," notes RV Industry Association President Craig Kirby.

LCI Industries Is A High-Growth Mid-Cap

LCI Industries is uniquely positioned within the RV market as the manufacturer of both aftermarket/retail and OEM equipment. The diversified strategy led to robust growth above and beyond the likes of Thor Industries and Camping World. On the top-line, revenue grew 41.2% from last year to just shy of $828 million and beat the consensus by 350 basis points. Revenue growth was driven by record demand in the retail RV segment as well as strong organic growth, acquisitions, and performance in the International segment. The after-market/retail segment saw the strongest growth, up 149%, with International and OEM trailing with gains of 69% and 11%.

"In the quarter, we significantly expanded market share across our businesses, supported by new business wins and content increases........we remain focused on executing our diversification strategy, capturing similar industry tailwinds in our aftermarket and adjacent industries markets," says president and CEO Jason Lippert.

Moving down to the bottom line the results are just as impressive. Adjusted earnings grew 76% YOY to come in at $2.72 and top consensus by $0.30. Net earnings came in two pennies below adjusted at $2.70 and topped by $0.28. Net earnings are up 91% from the previous year and are evidence the growth strategy is working. In terms of guidance, the company says preliminary October results are up 25% from last year due to significant increases in RV production and elevated retail demand.

LCI Industries Dividend Is Going To Grow

Looking to the balance sheet, this company is working hard to deliver shareholder value as well. The company has been using leverage to grow its business but even that is in good shape. Over the past quarter, the company ended the quarter with more cash and less debt than in the previous one. Cash increased by roughly $6 million to $68.2 million while debt declined a similar amount to $635.9 million. Total debt is down about 9.5% on a QoQ basis and expected to continue falling in the coming quarter.

As for the dividend, the stock is yielding about 2.65% with shares trading near $113 and I expect to see the distribution grow. The company has been increasing the payout for the last four years to $3.00 is still paying less than half of earnings to shareholders. The last increase was worth 15% and I think the next will be equally attractive. The only downside is the most recent increase was in the calendar 3rd quarter so the next will probably not come until late next year.

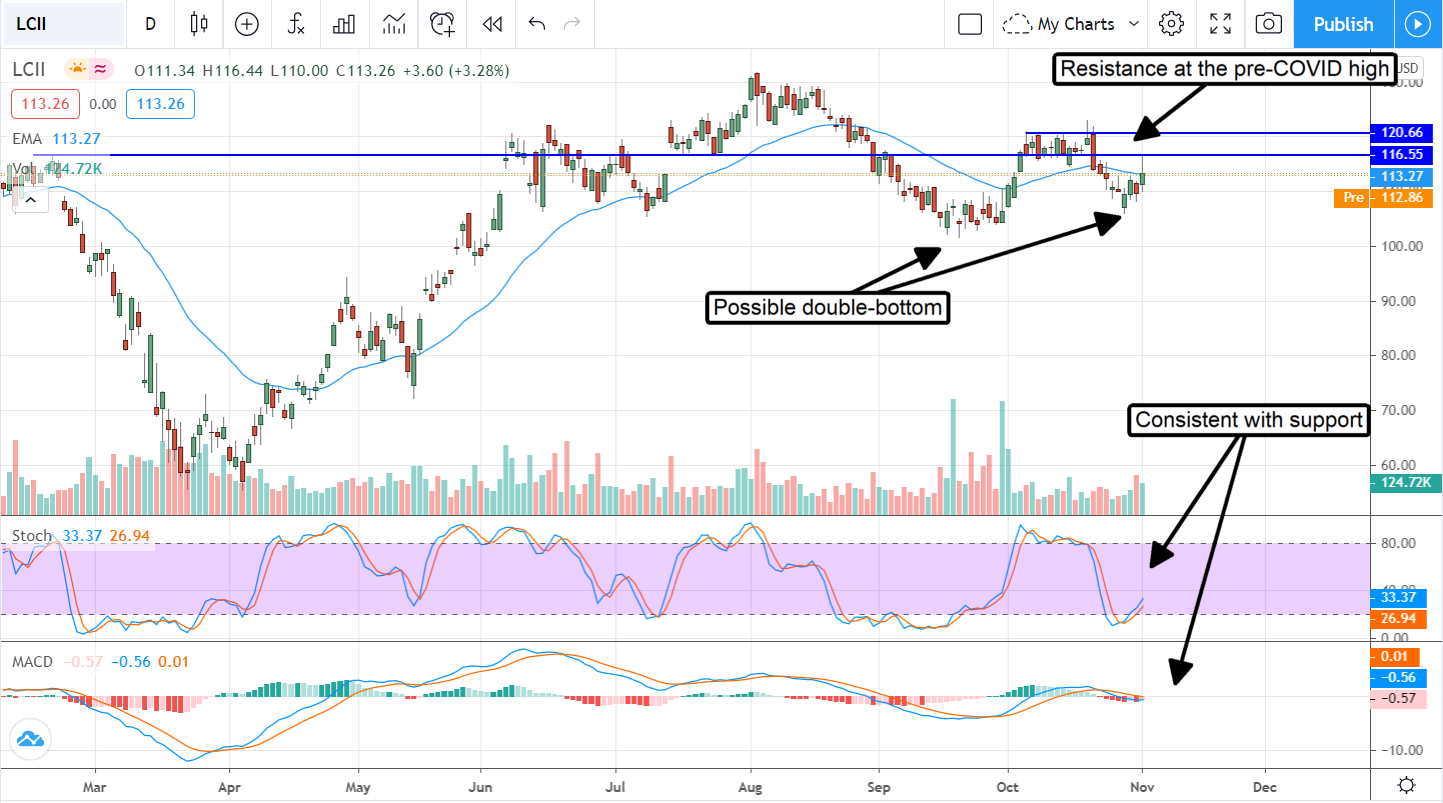

The Technical Outlook: A Buying Opportunity Is At Hand

Shares of LCII have been falling the last couple of months along with the broader RV industry. I think that move is played out. The data from LCI Industries, it’s competitors, and the industry is all bullish and points to rising share values over the next year. LCII is not the cheapest of the lot, that honor falls to Camping World, but it is a cheap stock relative to the broad market. Trading at 14X next year’s consensus (a consensus that is far too low given the results), the stock offers robust growth and a sleep-well-at-night high-yield dividend where most S&P 500 stocks don’t.

Looking at the chart, it is possible that LCII has already put in its bottom. The price action might be forming a double-bottom but it is too soon to trade on that signal. The indicators are consistent with support at this level but don’t yet confirm a reversal. The next hurdle will be the $120 level. If price action can get above that level we’ll probably see a new all-time high within the next few weeks.

Before you consider LCI Industries, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and LCI Industries wasn't on the list.

While LCI Industries currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Wondering when you'll finally be able to invest in SpaceX, Starlink, or X.AI? Enter your email address to learn when Elon Musk will let these companies finally IPO.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.