Tempur Sealy NYSE: TPX, a manufacturer and distributor of bedding products, has seen its shares quickly recover after tanking markets and fears of a retail slowdown sent shares from $100 in early February to $22 in mid-March.

At the onset of the pandemic, Tempur Sealy saw revenue collapse; during a few days in early April, sales plunged 80% compared to the same period a year ago. But since then, TPX’s business has recovered – and with it, the share price.

Tempur Sealy NYSE: TPX Q1 Earnings

Looking at Tempur Sealy’s Q1 earnings, the long-term strength of its business is apparent.

Net sales were up 19% yoy and adjusted EBITDA was up 63% yoy. This marks the fourth straight quarter of yoy EBITDA growth for TPX.

Its gross margin increased 260 basis points to 43.4% due to “higher unit volumes, lower commodity cost, and decreased floor model expenses.”

But the pandemic only started materially impacting business in mid-March, so these numbers aren’t indicative of TPX’s expected performance in a post-COVID environment.

The short stretch in early April was the worst time for TPX and as of the Q1 earnings call, April sales were down 55% month to date. But that is still a huge decrease, and Tempur Sealy tightened its belt to position itself for lean times ahead.

Tempur Sealy furloughed around 35% of its salaried workforce for 90 days and suspended its 401(k) match for the remainder of 2020. On top of that, the company delayed capital expenditures, eliminated nonessential expenses, and suspended its share repurchase. All in, TPX anticipates that these measures will save it around $300 million annualized.

As of March 31, Tempur Sealy had $197 million in cash and $100 million available under its revolving credit facility. None of its debt will mature until 2023. And at the time of the earnings call, the company still expected to generate operating cash flow in 2020. Since then, TPX’s outlook has only gotten better.

Tempur Sealy NYSE: TPX Q2 Guidance Boost

In mid-June, Tempur Sealy lifted its Q2 guidance. Shares gained more than 5% on the news after the market had already priced in substantial recovery.

After a weak April, sales have rebounded in May and early June. Tempur Sealy had expected sales to decrease 30% yoy in Q2; now it anticipates a 15% yoy decrease. Furthermore, the company now expects at least $50 million of unadjusted EBITDA for the quarter, with operating cash in the black.

Like many of the best-performing companies in the post-COVID world, Tempur Sealy has mitigated brick and mortar weakness with a growing e-commerce business. TPX’s e-commerce sales were up 125% quarter-to-date at the time of the announcement. And the wholesale channel is improving, providing less of a drag on results.

Tempur Sealy NYSE: TPX Valuation

TPX shares have more than tripled off the lows, but they are still below pre-pandemic levels. And with expectations for the company’s 2020 performance improving, its valuation looks appealing. Tempur Sealy is trading at (projected):

- 22x 2020 earnings

- 25x 2020 price-to-sales

- 15x 2021 earnings

- 14x 2021 price-to-sales

Tempur Sealy has seen modest top-line growth over the past few years, but when you consider the improvement in margins, shares start to look more appetizing. Obviously, there are limits to how much earnings can grow without high revenue growth, but it’s still a good sign.

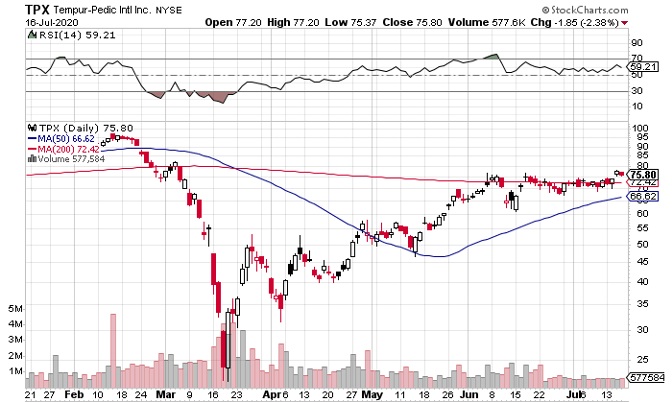

Tempur Sealy NYSE: TPX Technicals

Turning our attention to the chart, TPX looks like it’s consolidating for another leg-up.

In early June, shares stalled out at the 200-day moving average and spent a few trading sessions below it. Since the middle of June, shares have straddled the 200-day, never moving more than a few points above or below it. The 50-day moving average is now approaching the 200-day and looks like it will cross over in the next few weeks.

Volume has been noticeably light over the past few weeks, well below TPX’s average.

Over the past few trading sessions, shares have begun to clearly overtake the 200-day moving average, but volume has remained low, showing a lack of conviction. I see two near-term entry points:

- You can look for a pull-back of a few points to the 200-day moving average. Ideally, shares would dip a little below the moving average but close above the line, near the highs of the day, on high volume.

- Alternatively, if shares consolidate for a week or two around $73 to $76 and then breakout above the recent highs of $78 (on high-volume), you could get in there.

The key with TPX is to look for a high-volume move that shows conviction. The light-volume consolidation is fine – even positive – after such a big move off the lows. But you want to see some strong price action to indicate that there is the juice for another leg-up before getting in.

The Final Word

Tempur Sealy offers an excellent combination of strong fundamentals and positive price action. If the chart gives you the go-ahead, you should look to make a play.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Almost everyone loves strong dividend-paying stocks, but high yields can signal danger. Discover 20 high-yield dividend stocks paying an unsustainably large percentage of their earnings. Enter your email to get this report and avoid a high-yield dividend trap.

Get This Free Report