Texas Roadhouse NASDAQ: TXRH just had its second consecutive quarter of lower comps, right after recording

40 consecutive quarters of higher comps.

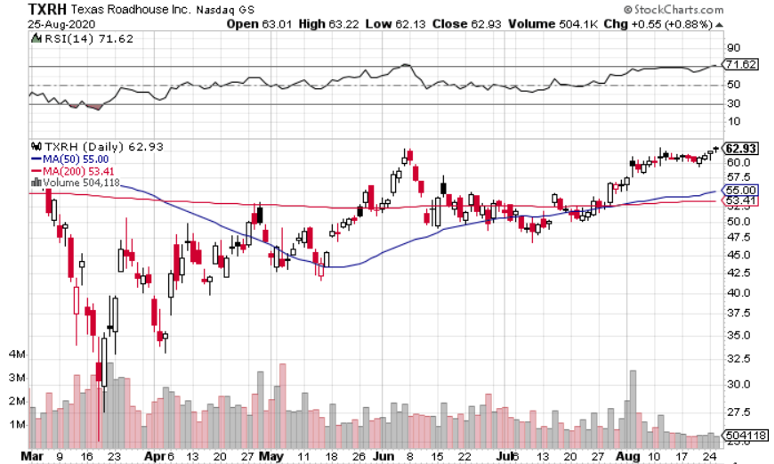

But TXRH is on the verge of a breakout from a three-month base and sits just 12.5% shy of its pre-pandemic highs.

How has Texas Roadhouse managed to pull this off? And should you look to get in?

TXRH is Making the Best of a Bad Situation

The pandemic has been harder on some industries than others. The restaurant industry has struggled mightily since March.

But Texas Roadhouse has outperformed its peers due to savvy management.

Stifel says, “The chain is benefiting from its booth-style seating and widespread partition installation (now in every restaurant), which can allow operating at nearly full capacity in certain jurisdictions. Furthermore, the company has erected temporary patios to further bolster capacity levels where possible."

Restaurants and retailers than can safely accommodate high numbers of people have fared relatively well since the onset of the pandemic.

In addition to maximizing capacity, Texas Roadhouse’s To-Go business has taken off. On the latest earnings call, CFO Tonya Robinson said, “The 499 restaurants operating under a limited capacity dine-in model generated average weekly sales of over $96,500 in June with To-Go sales accounting for roughly 25% of those sales. Our expectation based on recent trends is that we will continue to see this higher level of To-Go sales for the foreseeable future.”

Note that Texas Roadhouse has around 600 total restaurants.

Overall Revenue Beats Peers

In Q2, comps declined 32.8% yoy for the full quarter. But numbers improved each month, decreasing 46.7%, 41.9%, and 14.1% (all yoy) for April, May, and June respectively.

June seems to be a harbinger of things to come, with July comps decreasing 13% yoy.

The National Restaurant Association reported:

- June sales down 22.4% yoy at U.S. restaurants

- July sales down 19% yoy at U.S. restaurants

Texas Roadhouse has outperformed its peers since the onset of the pandemic.

Revenue Was in Line With Expectations And Earnings Exceeded Estimates

In Q2, Texas Roadhouse’s revenue came in at $476.4 million, down from $689.8 million in the year-ago period, and just below expectations for $477 million in revenue. The company reported a loss of $33.6 million, or 48 cents per share. That was down from a net income of 63 cents per share last year but beat expectations for a loss of 62 cents per share.

Texas Roadhouse’s strong balance sheet will allow it to easily weather the storm. And the company should return to profitability sooner rather than later.

The market reacted favorably to the earnings release – bidding shares up by around 4%.

TXRH looks primed for a leg-up when you consider its:

- Incredible long-term track record

- Outperformance of peers

- Ability to safely accommodate customers during the pandemic

- Strong balance sheet

- Bullish price action

TXRH is on the Verge of a Breakout

A little under a month ago, I recommended getting into TXRH on a decisive breakout above $55. A couple of days later, that breakout came to fruition. If you got in back then, you’d be up by more than 10%. But if not, don’t fret; TXRH is on the verge of a breakout from a longer-term base.

Look to get in if TXRH moves above $64 a share on high volume, ideally closing near the day’s highs.

The RSI just crossed into overbought territory, but I wouldn’t be overly concerned. TXRH is a bit extended on a near-term basis, but big picture, it isn’t.

On the plus side, the 50-day moving average recently crossed over the 200-day moving average, which is a sign of an emerging up-trend.

Outlook Remains Bright For TXRH

It would have been nice to get in around $55 a share, but it’s also comforting to see TXRH outperform in Q2. It’s increasingly clear that Texas Roadhouse will be one of the top-performing restaurants for as long as the pandemic lasts.

And once things do go back to normal, I’d expect Texas Roadhouse to start a new streak of higher comps. It probably won’t run off 40 consecutive quarters of comp growth again, but at around 28x projected 2021 earnings, it won’t have to in order to grow past its present valuation.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Looking to profit from the electric vehicle mega-trend? Enter your email address and we'll send you our list of which EV stocks show the most long-term potential.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.