Tesla NASDAQ: TSLA shares are up more than 10% following the Q1 earnings release, and they may move higher, but investors should not expect a sustained rally; they should only expect volatility. The news driving the market is good but so futuristic that it will not impact operations positively for at least twelve months. It is nothing more than a relief rally.

Among the drivers, no pun intended, are plans to build out a robotaxi fleet, the lean into AI, and cheaper models. Between then and now, the company faces many headwinds, including a tepid EV market, fierce competition, tightening margins, and negative cash flow.

The analysts' reaction aligns with the outlook for volatility. Analysts' activity is hot and mixed, but the takeaway is a headwind for share prices. More analysts are lowering their price targets than raising them, and more than one upgrade is needed to alter the consensus rating of Hold, verging on Reduce. The consensus target implies a 30% upside from the pre-release price action but is coming down quickly and a cap to any rally that may form. The takeaway is that Tesla is still a trader's stock and likely to make some wild swings within its trading range over the next few quarters.

Tesla Had a Tough Time in Q1

Tesla Today

$237.26 +9.76 (+4.29%) As of 02:18 PM Eastern

This is a fair market value price provided by Polygon.io. Learn more. - 52-Week Range

- $138.80

▼

$488.54 - P/E Ratio

- 116.03

- Price Target

- $290.66

Tesla is in no danger of implosion, but the Q1 results and outlook for the year suggest that the company’s struggles have yet to end. Q1 revenue fell 8.5%, the sharpest decline in over a decade, to $21.31 billion due to tepid demand growth, weak deliveries, and the impact of price and mix. The company issued numerous price cuts in most markets over the past twelve months, impacting the top and bottom lines. The company has issued new price reductions since the end of Q1, so they will continue to influence as the year progresses.

The impact of lower prices was felt worse on the bottom line. The company’s gross profit fell by 18% on a 200 bps contraction in margin compounded by higher costs. Operating margin fell by 592 basis points—income by 56% and adjusted earnings by 47%. The top and bottom lines were worse than forecast, with revenue 415 basis points short of the consensus reported by Marketbeat.com and earnings short by 1000.

The guidance is optimistic, but the optimism is offset by the continued expectation for weakness this year. In the company’s words, “In 2024, our vehicle volume growth rate may be notably lower than the growth rate achieved in 2023, as our teams work on the launch of the next generation vehicle and other products.” Let’s hope those products come to market in a reasonable time frame without unexpected costs. Tesla is more than a car company; an ecosystem is gaining leverage, but it takes cars to make it work.

Costs are also a problem. The company is leaning hard into its next growth phase, which depends on AI, autonomy, and the long-anticipated Model 2. FCF in Q1 came in at a long-term low of -$2.53 billion, resulting in a cash draw on the balance sheet. The company is well-capitalized but is going to burn cash this year.

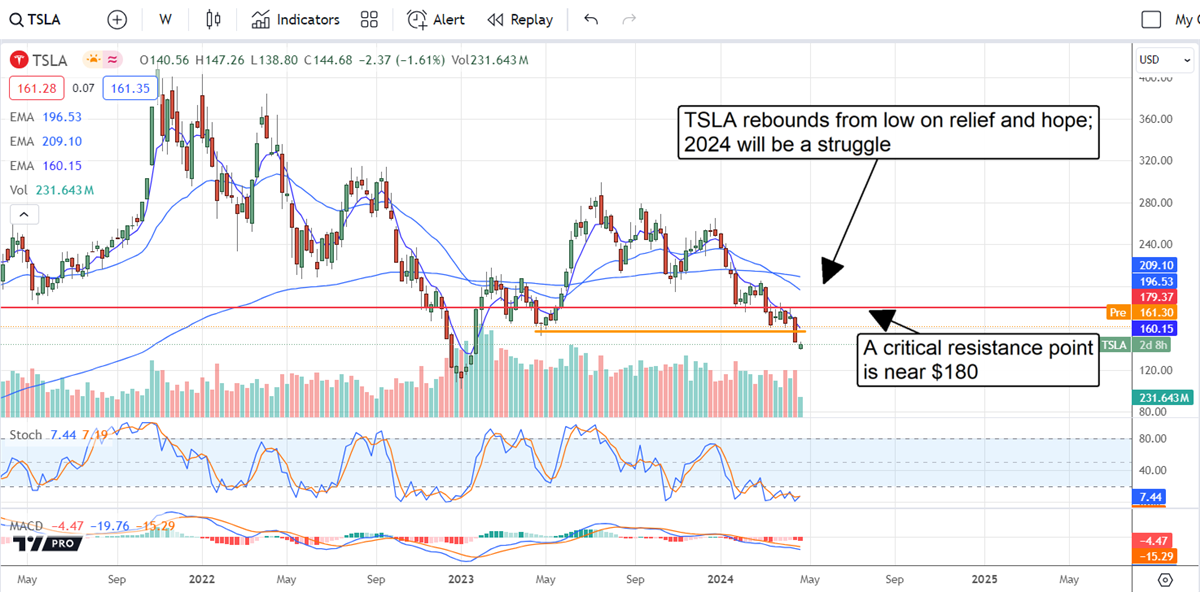

Tesla Rebounds: Significant Resistance Lies Ahead

The price action in Tesla has rebounded solidly following the report and may continue higher. The caveat is that this market is still below a critical resistance point that could cap gains. That point is near $180, and lows set in 2021. The $180 level has been a trigger point for buyers since then, and maybe again.

However, if this market cannot get above $180 and sustain it, the odds of a new low will grow. In that scenario, shares of Tesla will confirm resistance at a critical level and could fall as far as $115 before hitting solid support. Even if the market for TSLA can rise above $180, it will not be out of the weeds. The long-term 150-day EMA and longer-term 150-week EMA are just above and may also provide significant resistance to higher price action.

Before you consider Tesla, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Tesla wasn't on the list.

While Tesla currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

MarketBeat just released its list of 10 cheap stocks that have been overlooked by the market and may be seriously undervalued. Enter your email address and below to see which companies made the list.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.