Mall Retail Survives And On The Brink Of Thriving

With a broad economic reopening on the verge of unfolding it is only a matter of time before the mall retailers bounce back. Not to say the mall retail stocks haven’t been performing well only that their businesses are still struggling (in some cases) and that revenue should begin to accelerate significantly as soon as the second quarter of this year. With that in mind, we thought it was time to take a look at a couple of retailers that have not only survived the pandemic but gotten themselves into a position to thrive once it passes.

Kirkland’s Means Business

Mall-based lifestyle retailer Kirkland’s (NASDAQ:KIRK) reported what we view as a very positive Q4 report. The company’s $194.92 million in revenue is down 6.9% on a comp-basis but there is a mitigating factor that is not directly related to COVID. Kirkland’s closed 59 stores over the last year as part of its repositioning and brand-strengthening regimen. When adjusted for that the comps come in at a cool 1.8% with a noteworthy gain in the eCommerce channel. eCommerce sales grew by 35.5% over last year and helped to drive wider margins at both the gross and operating levels. Other highlights of the report include lower SG&A as a percentage of sales and positive GAAP eps of $1.36 versus a net loss in the year-ago period.

"We continue to carefully, deliberately and strategically evolve Kirkland's into a value-oriented specialty retailer. Our strategy has been to incrementally improve the quality and design of our merchandise while maintaining our opening price points and delivering value for our customers. Merchandising will be front and center again for us in 2021, along with leveraging the improvements in infrastructure and operating costs and accelerating our ongoing digital transformation. With total liquidity of $140 million at year-end, we are well-positioned to fund the evolution of Kirkland's,” noted CEO Woody Woodward.

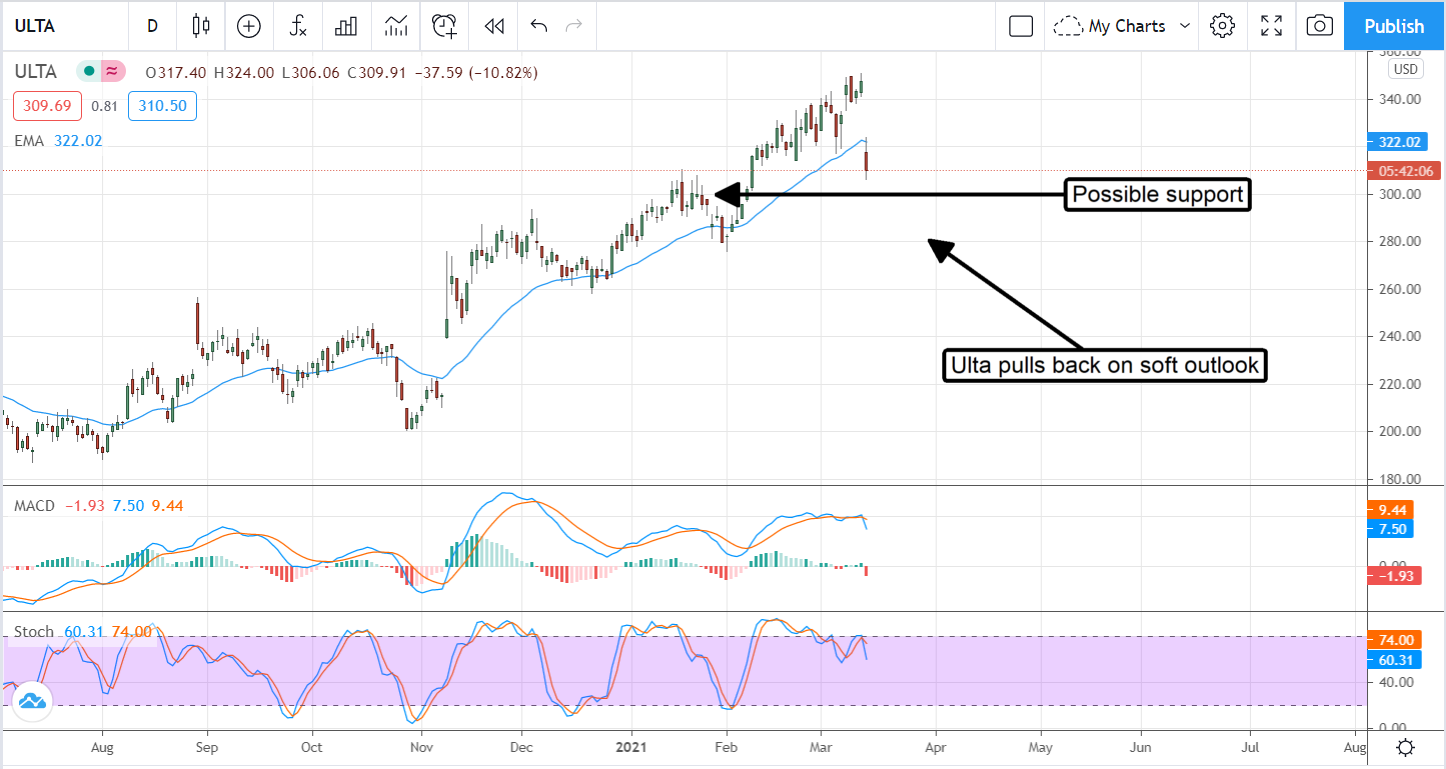

Ulta Growth Priced-In, Now Is The Time To Get Bullish

Ulta Beauty (NASDAQ:ULTA) reported a great quarter but one marred by a sickness that we’ve seen repeatedly over the last two weeks. Ulta Beauty’s great quarter was more than priced into the market and shares are down hard because of it. While not a great situation to be in if you already own Ulta and at higher prices it is a situation that begs the question, is it a good time to buy? Based on the fact that revenue and earnings are above consensus and the outlook for 2021 relatively robust we think the answer is yes.

The Q4 revenue of $2.2 billion and adjusted EPS of $3.41 both beat the consensus by a wide margin but were overshadowed by weak guidance. The company says it is planning on opening 40 new stores and upgrading 21 which should result in $7.2 to $7.3 billion in net revenue. This compares with the consensus of $7.31 billion and both are light in our estimations. The real factor that may be weighing on share prices is the retirement of its CEO who was largely responsible for the company’s growth over the past 7 years

Tilly’s Is Looking Good, Too

Tilly’s (NYSE:TLYS), like both Ulta and Kirkland’s, boasts a relatively strong cash position, low debt, and a strong balance sheet. What it has the others don’t is YOY growth and some expectation of a dividend. The company typically pays out an annual distribution that it declined to pay this year but is in a position to pay once the pandemic is over. Based on the 3.2% YOY growth that beat consensus by 100 basis points we think this company could easily increase the payout from prior levels as well.

Shares of Tilly’s are rocketing higher after the Q4 release and will likely continue higher unless there is a hiccup in the reopening. As of the last look, the stock was breaking above its 2019 highs and ready to move higher by as much as 25% over the next quarter. Longer-term, we expect this eCommerce winner in the young-adult lifestyle category will move up and eventually enter the $22 to $24 range.

Before you consider Tilly's, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Tilly's wasn't on the list.

While Tilly's currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Discover the next wave of investment opportunities with our report, 7 Stocks That Will Be Magnificent in 2025. Explore companies poised to replicate the growth, innovation, and value creation of the tech giants dominating today's markets.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.