Data storage solutions company

Western Digital NYSE: WDC stock has been collapsing since peaking at $78.19. The provider of data storage products had shares collapse even harder after rumors of a merger with the world’s second-largest NAND flash memory chip maker Kioxia may fall through as Kioxia pursues the IPO route. The Company had stellar fiscal Q4 2021 earnings and raised guidance, but shares continue to sell-off perhaps on

supply chain concerns that were noted in the conference call. The massive hunger for data storage is not slowing down as NAND memory prices continue to rise amidst

robust demand. While the Company benefits during the pandemic with

work-at-home,

gaming, and

cloud computing, the

reopening is causing a surge in enterprise HDD storage solutions. Prudent investors seeking a potential value play in the data storage segment can watch for opportunistic pullbacks in shares of Western Digital.

Q4 Fiscal 2021 Earnings Release

On Aug. 4, 2021, Western Digital released its fiscal fourth-quarter 2021 results for the quarter ending June 2021. The Company reported non-GAAP earnings-per-share (EPS) profit of $2.16 excluding non-recurring items versus consensus analyst estimates for a profit of $1.50, a $0.66 beat. Revenues grew 14.8% year-over-year (YoY) to $4.92 billion beating analyst estimates for $4.55 billion. Western Digital CEO David Goeckeler commented, "I am extremely proud of the outstanding execution our team exhibited as we achieved another quarter of strong revenue, gross margin and EPS results above expectations. Throughout this fiscal year, we successfully delivered both flash and hard drive innovations that are essential building blocks in the acceleration of the data economy. This innovation, combined with our broad channels to market, diverse end market exposure and improved operational efficiency, enabled us to successfully navigate through the pandemic and capitalize on strategic growth opportunities. We believe we have the right foundation for success - the right products, the right customer base, and the unique ability to address two very large and growing markets."

Raised Guidance

Western Digital raised its guidance for Q1 2022 with revenues estimated to come in between $4.9 billion to $5.1 billion compared to $4.91 consensus analyst estimates. The Company expected EPS between $2.25 to $2.55 versus $2.02 consensus analyst estimates.

Conference Call Takeaways

CEO Goeckeler set the tone, “The upside was primarily driven by record demand for our capacity enterprise hard drives. Fiscal year 2021 revenue totaled $16.9 billion, and we reported non-GAAP earnings per share of $4.55. Last March I joined Western Digital with a strong conviction in the digital transformation that is reshaping every industry, every company, and every person's day-to-day life. At that time, we were in the early stages of the pandemic. Today the accelerated digital transformation that has occurred during this period has created a world that is more technology enabled and technology dependent than ever before. The increasing value and importance of data is undeniable and Western Digital will continue to capitalize on this opportunity as the only provider of both flash and hard drive solutions. Our ability to provide this diverse range of technologies enables us to drive innovation from endpoints to the edge to the cloud and combined with our commitment to delivering the highest quality products, is ultimately what sets us apart and allows us to deliver strong results.”

SSD

CEO Goeckler provided a recap of flash and HDD businesses, “Within data center devices and solutions demand for our NVMe enterprise SSDs came in above our expectations, achieving strong quarter-over-quarter revenue growth, we are pleased with our progress in enterprise SSDs as we completed the qualification of another cloud Titan and are ramping the product more broadly. Within client SSD, we experienced revenue growth as demand remained strong for notebooks and Chromebooks. This remains a large growing and an important end market for Western Digital across our OEM channel and retail routes to market. Within gaming, demand from the latest generation of game consoles, and our WD Black product line was robust as gamers continued to prefer our expanding lineup of customized solutions.”

Hard Drives

He continued, “In HDD, we had our highest organic sequential revenue growth in the last decade, driven by the successful ramp of our 18-terabyte energy-assisted hard drive, growing cloud demand, a recovery in enterprise spending, and to a lesser extent crypto currency driven by Chia. This impressive performance is a reflection of our data center customers confidence in our innovation engine for capacity enterprise hard drives. Shipments for our 18teribyte hard drive nearly tripled sequentially, highlighting our leadership in the latest capacity point and the leading edge energy-assist technology underpinning it. These drives are fully commercialized we expect the 18 terabyte hard drive to be the workhorse for the fiscal year. I'm excited to announce a record shipment of over 104 exabytes in capacity enterprise hard drives, a 49% increase sequentially. This is a significant achievement for the business as we have all of our largest customers qualified and are well into ramping our energy-assisted hard drives. In addition, client demand for desktop and smart video has been strong throughout the quarter due to improving OEM demand. While we are actively managing supply constraints, we expect strength in OEM to continue in the fiscal first quarter. Within retail HDD demand was above expectations as we saw consumer interest grow for both at home HDD storage and for smart video applications.”

Supply Chain Concerns

CEO Goeckeler concluded, “While we remain optimistic, there are several factors we are closely monitoring. Most importantly, we are actively managing the continued impact of the pandemic. The disruptions to the supply chain have presented a challenge across the industry and we continue to see shortages of certain components. Additionally, logistics remain a challenge as different geographies are in various stages of reopening. This has been a major contributor to increase lead times and may pose challenges in the future. As a result of the supply disruptions, logistics challenges and increased lead times, we continue to face additional cost pressures. Despite these obstacles, we are working diligently to continue delivering to our customers while maintaining a disciplined approach to pricing.”

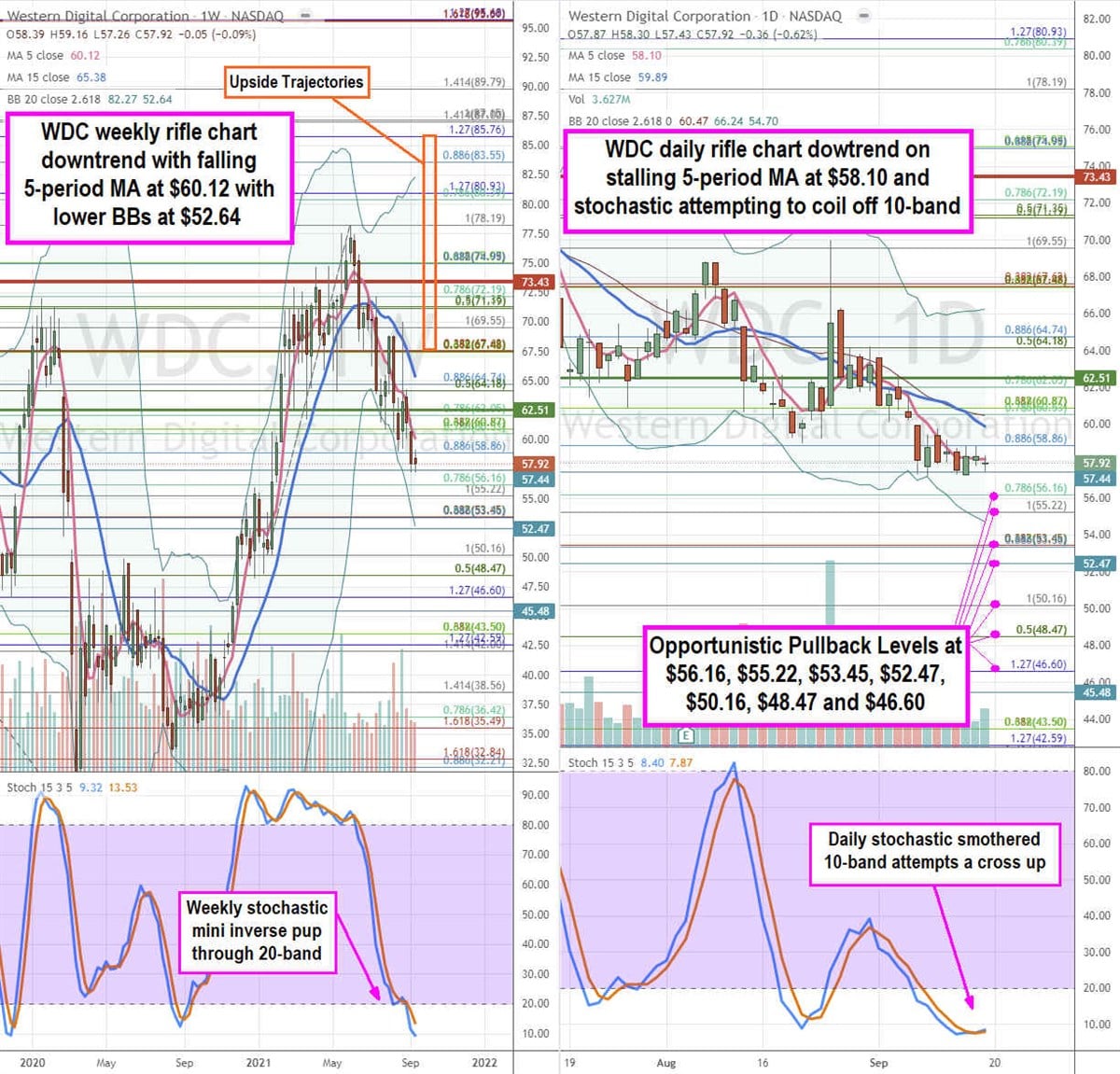

WDC Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provides a precision view of the price action playing field for WDC shares. The weekly rifle chart peaked near the $78.19 Fibonacci (fib) level before plunging into the $57s. The weekly downtrend was triggered on the market structure high (MSH) sell trigger on the breakdown under $73.43. The weekly downtrend has a falling 5-period moving average (MA) at $60.12 followed by the falling weekly 15-period MA at $65.38. The weekly lower Bollinger Bands (BBs) sit at $52.64. The weekly stochastic failed the coil attempt off the 20-band and crossed back down through the 20-band indicating an oversold situation. The daily rifle chart has also been in a downtrend that is starting to slow down as the daily 5-period MA stalls at $58.10 but the 15-period MA is still falling at $59.89. The daily lower BBs sit at $54.70. The daily market structure low (MSL) buy triggers on a breakout through the $62.51 level. Prudent investors can monitor for opportunistic pullback levels at the $56.16 fib, $55.22 fib, $53.45 fib, $52.47 level, $50.16 fib, $48.47 fib, and the $46.60 fib. The upside trajectories range from the $67.48 fib up towards the $85.76 fib level.

Which stocks are likely to thrive in today's challenging market? Enter your email address and we'll send you MarketBeat's list of ten stocks that will drive in any economic environment.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.