Residential home builder

Toll Brothers NYSE: TOL stock has been unstoppable in 2021 with a strong housing market despite rising materials costs. Shares rebounded sharply on its blowout fiscal Q4 2021 earnings results. The Company raised its guidance even after the $0.52 per share earnings beat.

Supply chain disruption and

labor constraints have impacted the timing of home deliveries later than expected, but backlog remains strong at $10.5 billion. Despite the Federal Reserve forecasting at least

two rate hikes in 2022, the demand for residential housing continues to be strong driving

growth. Prudent investors looking for exposure with a top residential home builder can watch for opportunistic pullbacks in shares of Toll Brothers.

Q4 Fiscal 2021 Earnings Release

On Dec. 7, 2021, Toll Brothers released its fiscal fourth-quarter 2021 results for the quarter ending October 2021. The Company reported earnings-per-share (EPS) profits of $3.02 beating consensus analyst estimates for a profit of $2.50, a $0.52 beat. Revenues grew 19.5% year-over-year (YoY) to $3.04 billion, beating consensus analyst estimates for $2.91 billion. Home sales revenues were $2.95 billion, up 18% YoY. Delivered homes rose 14% to 3,341, falling short of prior guidance of $3,450. Backlog value grew 49% to $9.5 billion with 10,302 homes, up 32%.

CEO Comments

Toll Brothers CEO Douglas Yearley Jr. commented, “We are very pleased with our fourth quarter results, which cap an extraordinary year of record revenues, earnings, contracts and backlog value for Toll Brothers. In the fourth quarter, we grew home sales revenues by 18%, achieved an adjusted gross margin of 25.9%, and nearly doubled our pre-tax income and earnings per share from one year ago. In addition, we continued to improve the capital efficiency of our land acquisition strategy, with optioned lots now representing 55% of our 80,900 total lots at quarter end, up from 43% one year ago. Our fourth quarter results, combined with our strategy of driving capital and operating efficiency, contributed to an 830 basis point increase in our full year return on beginning equity to 17.1%. Demand remains very strong. The housing market continues to benefit from solid fundamentals, including favorable demographics, pent up demand from over a decade of underproduction of new homes, low mortgage rates, a tight resale market, and permanent changes to the way Americans view life, work, and home. We believe these trends will continue to drive strong demand for our first-time, move-up and active adult communities well into the future.”

He continued, “We, like the rest of the industry, continue to be challenged by significant supply chain and labor constraints that are extending delivery times for our homes. Notwithstanding these issues, which we expect to continue for the foreseeable future, we project 20% revenue growth in FY 2022. In a year of record sales, we increased our community count by 7% to 340 communities at fiscal year-end. We continue to project 10% community count growth by FYE 2022 and currently own or control enough land for additional meaningful growth in FY 2023. Based on the strong pricing embedded in our all-time record backlog of $9.5 billion, we project a 250 basis point improvement in full year adjusted gross margin, which we expect to be second half weighted as peak lumber prices from the spring of 2020 flow through our first half deliveries. Driven in part by our permanent pivot to a more capital efficient land strategy, we are also projecting a further significant increase in our return on beginning equity to well over 20%.”

Upside Guidance

The Company issued upside fiscal full-year 2022 guidance estimates for 20% revenue growth at $10.55 billion versus $10.32 billion consensus analyst estimates. The Company noted that significant supply chain issues and labor constraints have been extending delivery times for homes. Fiscal 2022 home deliveries are expected between 11,250 units to 12,000 units with fiscal Q1 expected to deliver 2,000 units.

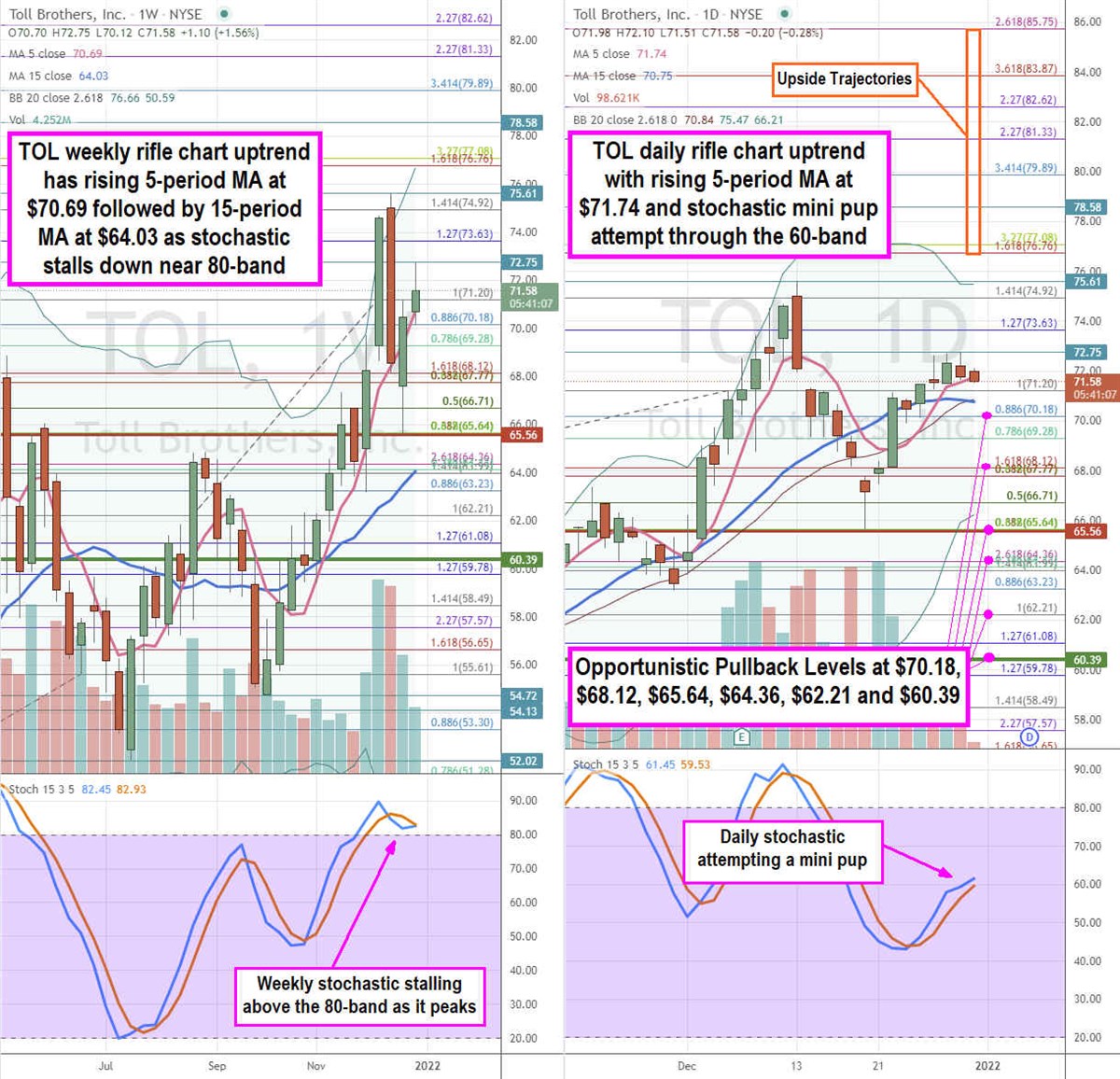

TOL Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provides a near-term precision view of the price action playing field for TOL shares. The weekly rifle chart peaked at $75.61 and fell to the $65.64 Fibonacci (fib) level on the market structure high (MSH) trigger at $65.56 test before snapping back up. The weekly rifle chart resumed its uptrend as share spiked back up through its rising 5-period moving average (MA) at $70.69 followed by its rising 15-period MA at $64.03. The weekly uptrend started on the weekly market structure low (MSL) buy triggered above $60.39. The weekly upper Bollinger Bands (BBs) sit near the $76.76 fib level. The weekly stochastic initially crossed down and stalling above the 80-band to set up a make or break situation. The daily rifle chart breakout is attempting to form a stochastic mini pup if the daily 5-period MA holds at $71.74. Meanwhile, the 15-period MA went flat at $70.75. The daily upper BBs on a mini pup sit at $75.47. Prudent investors can watch for opportunistic pullback levels at the $70.18 fib, $68.12 fib, $65.64 fib, $64.36 fib, $62.21 fib, and the $60.39 fib level. The upside trajectories range from the $76.76 fib up towards the $85.75 fib level.

Before you consider Toll Brothers, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Toll Brothers wasn't on the list.

While Toll Brothers currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Learn the basics of options trading and how to use them to boost returns and manage risk with this free report from MarketBeat. Click the link below to get your free copy.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.