A Restaurant By Another Model …

Shares of Dunkin Donuts (DNKN) have not been immune to the global pandemic. The company’s share price corrected more than 50% from its 2020 high outpacing the broader-market. The reason is simple, the pandemic put the fear of God into the market and sparked a round of panic-selling the likes of which I’ve never seen before. Restaurant stocks like Dunkin Donuts were among the worst hit because their business model’s put people at risk.

On the flip-side, shares of Dunkin (among other fast-food oriented names) only corrected 50% where others in the group are still bleeding. Shares of sit-down establishments like Cracker Barrel (CBRL), Cake Factory (CAKE), and Ruth’s Chris (RUTH) corrected more than 50%, more than 60% in some cases, and look like lower lows are on the way.

This Is What Sets Dunkin Donuts Apart From The Crowd

Dunking Donuts received a double-upgrade this morning from analysts at Credit Suisse. The move is despite an expectation for high-double digit declines in comp-store sales and predicated on the company’s position within the market. The firm says Dunkin’s 100% franchised model sets it apart from its peers and warrants a premium in today’s market.

“We see limited risk of mass closures given the health of its franchisee system, attractive category dynamics, what appears to be broad eligibility for franchisees to take advantage of benefits from the government stimulus and high US exposure (nearly 90% of operating profit)."

Credit Suisse raised the rating for Dunkin by two notches to outperform from underperform because of their view. Their price target is $67, below the $75 consensus and a 15% premium to Friday’s closing price.

Credit Suisse isn’t the only analyst to be bullish on Dunkin either, eight of the 28 analysts with current ratings have the stock at a buy or higher while only 1 is bearish. Because most analysts are neutral there is a lot of fuel for an upgrade-driven rally once the company proves itself via earnings.

"In our opinion, off-premise, domestic- skewed franchise models of DPZ and DNKN continue to represent defensive near-term BUYs," writes analyst Matthew DiFrisco of Guggenheim We reiterate our BUY rating and lower our PT to $71 from $86, applying a 17.1x recovery multiple on our 2021E EBITDA of $488.7mm... The NT premium to shares, in our view, is justified in the current market given the domestic growth potential, high return/CF franchise model, and improving digital integration.”

A Sweet Dividend To Enjoy With Your Coffee Stock

Dunkin Donuts is expecting to take a hit to revenue and earnings in 2020 but it shouldn’t impair the dividend. The $2.77 consensus EPS is about 25% below the previous year but leaves the company’s payout ratio at a very reasonable 58%. Looking forward, EPS and revenue growth should resume next year with earnings surging 17% putting dividend coverage near 200%.

At today’s share prices the stock is paying about 2.80% yield. The company has a history of distribution increases, eight years, so there is some expectations for another increase later this year. The company just upped the payout with the last distribution so it won’t come until the fourth quarter if it does.

Dunkin is carrying some debt on the balance sheet but not a crippling amount and virtually all long-term in nature. With the company’s cash position, cash flow, and coverage ratios I see no reason at this time why another distribution increase won’t be forthcoming.

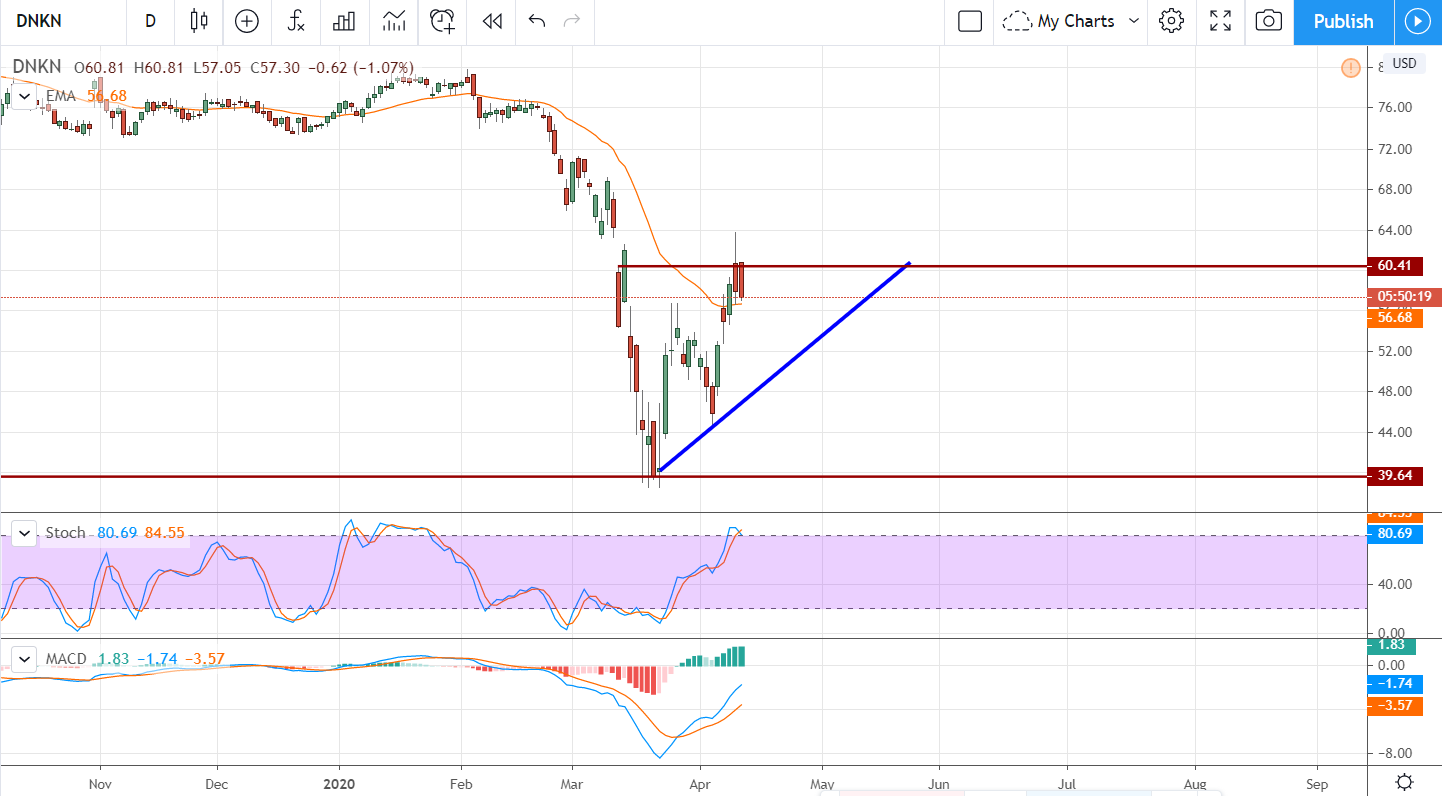

The Technical Outlook: A Reversal Is In-Play

Dunkin wasn’t immune to the pandemic-driven sell-off but it is recovering quickly. The stock has rebound more than 50% off its lows and recovered more than 50% of the losses it experienced in March. The price action bounced strongly from the four-year low and has since tested for support and confirmed its presence. The price pattern smacks of double-bottoming, a slightly-off kilter double-bottom that is supported by the indicators.

The indicators, both MACD and stochastic, are showing what would be strong signals if the stock had been trending bullishly before the correction began. As it is, the signals are strong but may mean little more than a new trading range has been established. There is resistance at the $60 level that may keep price action in check if the company can not produce satisfactory results. Dunkin is expected to report Q1 earnings in about two weeks so there won’t be too long to wait.

Until then, the bias is bullish and price action is showing support at the short-term moving average. This suggests a rally is brewing that may be unleashed by the EPS report. A move up above the $69 level would be bullish if supported by the report, a move that could take prices back up to retest February highs. If not, investors may be able to get a second entry at a lower price.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Options trading isn’t just for the Wall Street elite; it’s an accessible strategy for anyone armed with the proper knowledge. Think of options as a strategic toolkit, with each tool designed for a specific financial task. Get this report to learn how options trading can help you use the market’s volatility to your advantage.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.