Walmart Today

$95.12 +2.32 (+2.50%) As of 03:04 PM Eastern

- 52-Week Range

- $58.56

▼

$105.30 - Dividend Yield

- 0.99%

- P/E Ratio

- 39.47

- Price Target

- $103.58

Walmart's NYSE: WMT February price correction is a buying signal for long-term investors. The drop is due to slowing growth and tariff fears but does little to alter the long-term outlook for earnings, cash flow, equity gains, and capital return. While slower growth and tariffs are headwinds for retailers, consumers remain strong, and the business remains solid, leaving the company to do what it does best: manage its supply chain and provide compelling value for consumers.

The tariff threat is real, but it is not new. The company has been navigating a tariff-laden environment since the first Trump administration and is prepared to mitigate the impact of new tariffs to a degree. Less than 35% of the company’s products come from outside the U.S., minimizing exposure that can be further reduced through strategic sourcing and private labels.

Walmart Has Strong Q4, Issues Cautious Guidance for Calender 2025

Walmart had a strong FQ4 2025/CQ4 2024 with revenue of $180.6 billion, rising by 4.1% and outpacing MarketBeat’s reported consensus by nearly 100 basis points. Critical details include strength in the core U.S. market and broad strength across categories offset by marginal weakness Internationally. Sales at Walmart U.S. rose by 5% on a 4.6% comp increase, a 2.8% increase in ticket count, and a 1.8% increase in ticket size. Sam’s Club was also strong, driven by a robust 13% increase in membership income. Sales at Sam’s rose by 5.7% on a 5.4% increase in transactions and a 1.3% increase in ticket size.

Walmart MarketRank™ Stock Analysis

- Overall MarketRank™

- 88th Percentile

- Analyst Rating

- Moderate Buy

- Upside/Downside

- 9.2% Upside

- Short Interest Level

- Healthy

- Dividend Strength

- Strong

- Environmental Score

- -2.08

- News Sentiment

- 0.63

- Insider Trading

- Selling Shares

- Proj. Earnings Growth

- 18.43%

See Full AnalysisThe margin news is also good. The company widened its gross and operating margin to drive leveraged growth on the bottom line and outperformance relative to analysts' forecasts. The net result is $0.66 in adjusted EPS for a gain of 1000 BPS, nearly double the top-line growth, with strength expected to continue in F2026.

The problem is that the guidance is weaker than forecasted but likely cautious due to consumer trends. The company forecasts only 3% to 4% revenue growth compared to the 4.2% expected by analysts, cautious because of labor market strength and retail sales data. The latest data shows persistently strong job growth, declining unemployment, and average wages rising more than 4%, underpinning a 4.2% increase in retail sales. These trends are expected to continue in F2026 and may gain momentum later in the year as Trump’s policies spur domestic activity.

Walmart Capital Return Is Safe for 2025

Walmart’s investment attraction includes the capital return program. Neither the dividend distribution nor buybacks are significantly large, but together, they amount to more than 1% annualized return with shares near $100 and are sustainable. The dividend is worth less than 35% of the F2026 earnings outlook, including the 13% increase announced for the year; it yields about 0.8% and is compounded by buybacks. The buybacks reduced the count by 0.3% in 2024 and will likely reduce it by a similar amount in F2026.

Regarding the balance sheet, it is as healthy as ever. At the end of F2026, the highlights include reduced cash offset by increased inventories, receivables, and assets and reduced debt. The net result is a nearly 8% increase in shareholder equity and low business leverage. The long-term debt is about 0.35X equity.

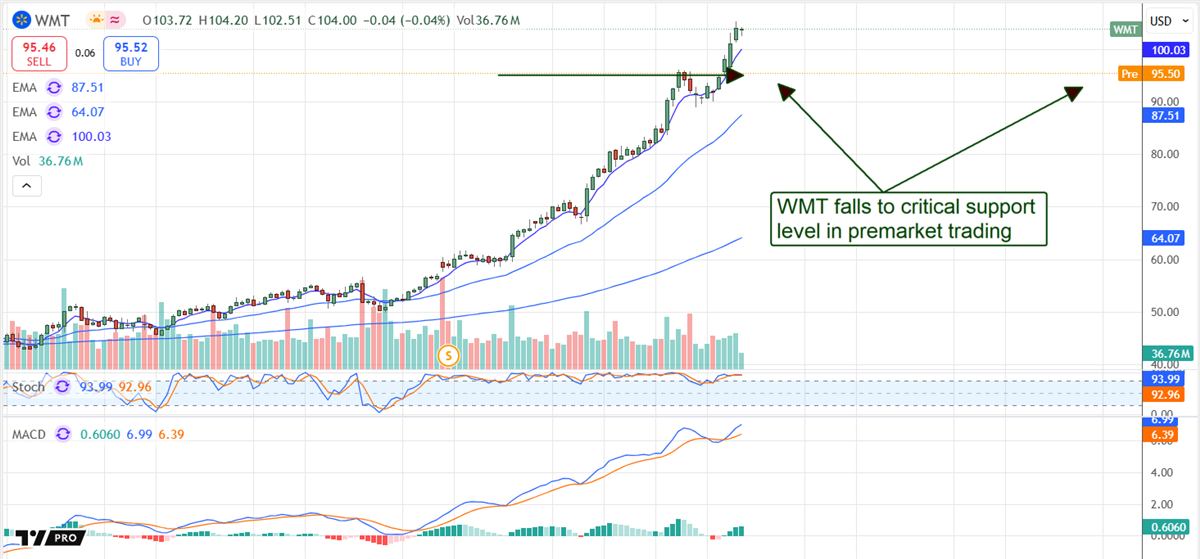

Walmart Pulls Back to Critical Support Level

After the guidance update, Walmart’s share price fell more than 8% in premarket trading but may not fall much further. The move put the market at a critical support level near $95, likely to trigger buying if not a rebound in action. Assuming the market confirms support at this level, Walmart’s stock will likely move sideways within a new range until later in the year. If support is not confirmed at this level, Walmart’s stock could fall to $90 or lower before hitting solid support.

Before you consider Walmart, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Walmart wasn't on the list.

While Walmart currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Which stocks are likely to thrive in today's challenging market? Enter your email address and we'll send you MarketBeat's list of ten stocks that will drive in any economic environment.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.