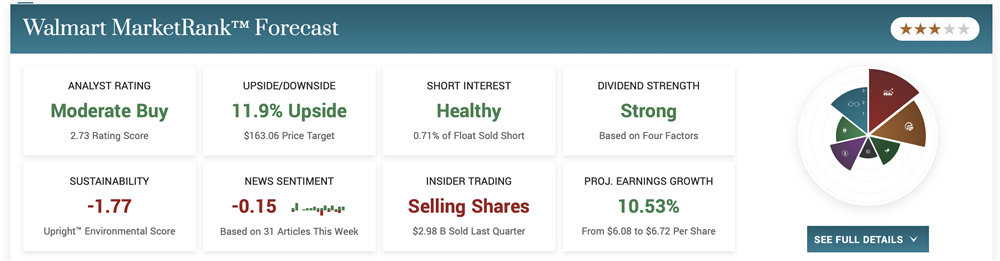

Evercore ISI analysts upgraded Walmart NYSE: WMT in the final days of March from In Line to Outperform (or Moderate Buy). The upgrade accompanied a target price increase from $145 to $160 per share. Apparently, analysts foresee potential/future traffic and margins expanding for at least the next two years.

In their note about the upgrade, analysts said it is evident that traffic will turn and that turn will be broad. They comment, “With consumers across the demographic spectrum making wallet allocation choices after several years of record nominal retail spending, Walmart is poised to regain share."

The analyst note continues, "With traffic momentum and margin expansion likely amidst a decelerating Retail world, we like Walmart's scale, balance sheet, and stability.”

So let’s look at Walmart’s scale, balance sheet, and stability compared with its peers.

What is There To Like About Walmart’s Scale?

Walmart already has 11,300 stores across 20 countries, offering even more products exclusively online. They employ 2.1 million employees worldwide, with 1.6 million in the US. Approximately 90% of the US population lives within 10 miles of a Walmart store. They also have 800+ global Sam’s Club locations.

With a market capitalization of $391.57 billion, the only sizable competitor worth more is Amazon.com, Inc. NASDAQ: AMZN, whose market cap is $1.05 trillion. That said, AMZN’’s annual dividend is only $0.20 with a yield of 0.20%, while WMT is paying out $2.28 at a 1.60% yield. More importantly, WMT has seen consecutive annual dividend increases for 51 years.

Peers like Costco NASDAQ: COST and Target NYSE: TGT are doing much better than Amazon compared to Walmart’s scale, though WMT remains attractive. COST’s $217.96 billion market cap is notably smaller than WMT, but its average volume is also significantly lower, at only 1.96 million. WMT does about 6.48 million trades a day, on average. Costco’s $3.60 dividend is higher, but the yield is only 0.70%. On the other hand, Target has a $73.78 billion market capitalization and pays out the highest dividend, at $4.32 (at a yield of 2.7%), though they’ve had only seven consecutive annual increases.

What is There To Like About Walmart’s Balance sheet?

Here are a few key factors to consider regarding the balance sheet:

- Operating revenue has grown by 2.3% YoY, on average, for ten years, now at $611,289.0

- Gross profit also grew 2.3%, on average, for the last ten years

- Net income $11.68 billion

- Total current assets equal 243,197, about 10% above the 10-year average

- Consolidated net income (loss) fell 2% last year, the lowest since 2019

- While 4.27 [basic and diluted] EPS is down from the previous three years, it is still in the higher half of the range of the last ten years

- P/S 0.64

WMT is currently growing at least 2.5% on average across all metrics. This may not seem like a big deal, but at this pace, they should easily make up the 3.76% they are currently down since last year. Of course, this could also be the potential catalyst for new momentum.

What is There to Like About Walmart’s Stability?

Finally, WMT is the most stable stock among its nearest competitors, with a 0.48 beta value. This makes WMT 52% less volatile than the S&P 500 Index. And the S&P is already up 4% since the top of the year. That could be an indication that WMT will see similar success. By comparison, Costco and Target have beta values of 0.79 and 1.05, respectively. Amazon’s beta value is 1.25.

At the close of March, WMT share value sits comfortably in the upper 40% of the 52-week range. The current trading volume is only slightly above the 6.54 million daily average. Among the peer group introduced earlier, WMT has better standing despite all having the same rating. COST, for example, is in the bottom 40% of the 52-week range, with trading volume under the 1.96 million average. And at $491.48 per share, COST is pricey compared to WMT.

Similarly, TGT is a Moderate Buy in the bottom 30% of the 52-week range. Its volume is currently about one-third of its daily average. Its $160.27 share price isn’t too bad, but AMZN shares are only $102.00. AMZN is also a Moderate Buy even though its value is in the bottom 25% of the 52-week range.

Finally, while WMT is down 2.8% Year over year, the stock continues to outperform the general retail sector, down 13.31%. WMT is also doing better than the whole of the NYSE, which is down 13.54%. In all, it would appear there is a lot of evidence to support the analyst upgrade.

Before you consider Walmart, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Walmart wasn't on the list.

While Walmart currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Wondering when you'll finally be able to invest in SpaceX, Starlink, or X.AI? Enter your email address to learn when Elon Musk will let these companies finally IPO.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.