Data storage solutions company

Western Digital NYSE: WDC stock may have bottomed out after its fiscal Q1 2022 earnings shortfall and lowered guidance. COVID-19 impact,

chip shortage and

supply chain disruptions all played a part in the transitory shortfalls to set the bar lower moving forward. Supply disruption caused its flash and hard drive business units to decline sequentially. Shares are trading at a 6.5 forward P/E, making it a chance opportunity to get in at bargain value levels assuming the

supply chain constraints are temporary. The insatiable demand for

data storage will continue to accelerate as cloud migration continues, especially if the

metaverse becomes a reality. Prudent investors can watch for opportunistic pullbacks in shares of Western Digital for exposure.

Q1 Fiscal 2022 Earnings Release

On Oct. 28, 2021, Western Digital released its fiscal first-quarter 2022 results for the quarter ending September 2021. The Company reported non-GAAP earnings-per-share (EPS) profit of $2.49 excluding non-recurring items versus consensus analyst estimates for a profit of $2.44, a $0.05 beat. Revenues grew 28.8% year-over-year (YoY) to $5.05 billion falling short of analyst estimates for $5.06 billion. Western Digital CEO David Goeckeler commented, “Strong demand across diverse end markets, particularly for our cloud products, combined with Western Digital’s strong innovation engine, broad routes to market and sharpened execution, enabled us to deliver solid results within our guidance range, even in the face of significant COVID impacts and supply chain disruptions. While these disruptions are transitory, the long-term opportunities for Western Digital remain unchanged as the world’s digital transformation continues to accelerate. We believe that the migration to the cloud and demand for storage solutions throughout the client and consumer markets will continue to drive a huge opportunity for Western Digital and our customers.”

Lowered Guidance

Western Digital lowered its guidance for Q1 2022 with revenues estimated to come in between $4.70 billion to $4.90 billion compared to $5.24 billion consensus analyst estimates. The Company expected EPS between $1.95 to $2.25 versus $2.63 consensus analyst estimates. Operating margins are expected between 32% and 34%/

Conference Call Takeaways

CEO Goeckeler set the tone, “This marks the sixth quarter in a row of meeting or exceeding guidance, a point that we are particularly proud of as we continue to navigate uncertainty and volatility in the market. Strong demand across diverse end markets, particularly for our cloud products combined with Western Digital strong innovation, broad routes to market, and sharpen to execution enabled us to deliver results within our guidance range despite significant COVID impacts and supply chain disruptions. While these disruptions are transitory, the long-term opportunities for Western Digital remain unchanged as the world's digital transformation continues to accelerate. During the quarter, we shipped a record level of exabytes, while also improving non - GAAP gross margin across both flash in HDD and generating profitable growth. We saw a strong demand for our latest generation hard drives and flash products in the Cloud end market, as well as strong consumer demand for new 5G based mobile phones incorporating our latest fixed Five Flash Solutions. The strong demand for these products were partially offset by pressure in the commercial channel within the client end market and certain portions of the consumer end market, particularly retail. This was attributable to component issues impacting our customers’ ability to ship products, greater component sources constraints within our own operations, and uneven geographic demand due COVID lockdowns. Our continued focus on innovation and a more agile business unit structure enabled us to quickly adapt to these dynamics.”

He concluded, “Our long-term goal is to grow BiCS in line with the market taking advantage of our product and end market breadth to shift our BiCS to optimize profitability. As we look into calendar year 2022, we are optimistic as our customers continue to indicate strong end demand across Cloud, client, and consumer end markets. We have industry-leading technology, the right product portfolio, and an investment in the organizational agility to fundamentally drive improved profitability regardless of market conditions. We have a great position in two large and growing markets in Flash and HDD. And we have proven our ability to drive innovation throughout our portfolio and deliver industry-leading products to a broad and loyal customer base. We believe that the migration to the Cloud, in demand for storage solutions throughout the client and consumer markets will drive a huge opportunity for Western Digital and our customers.”

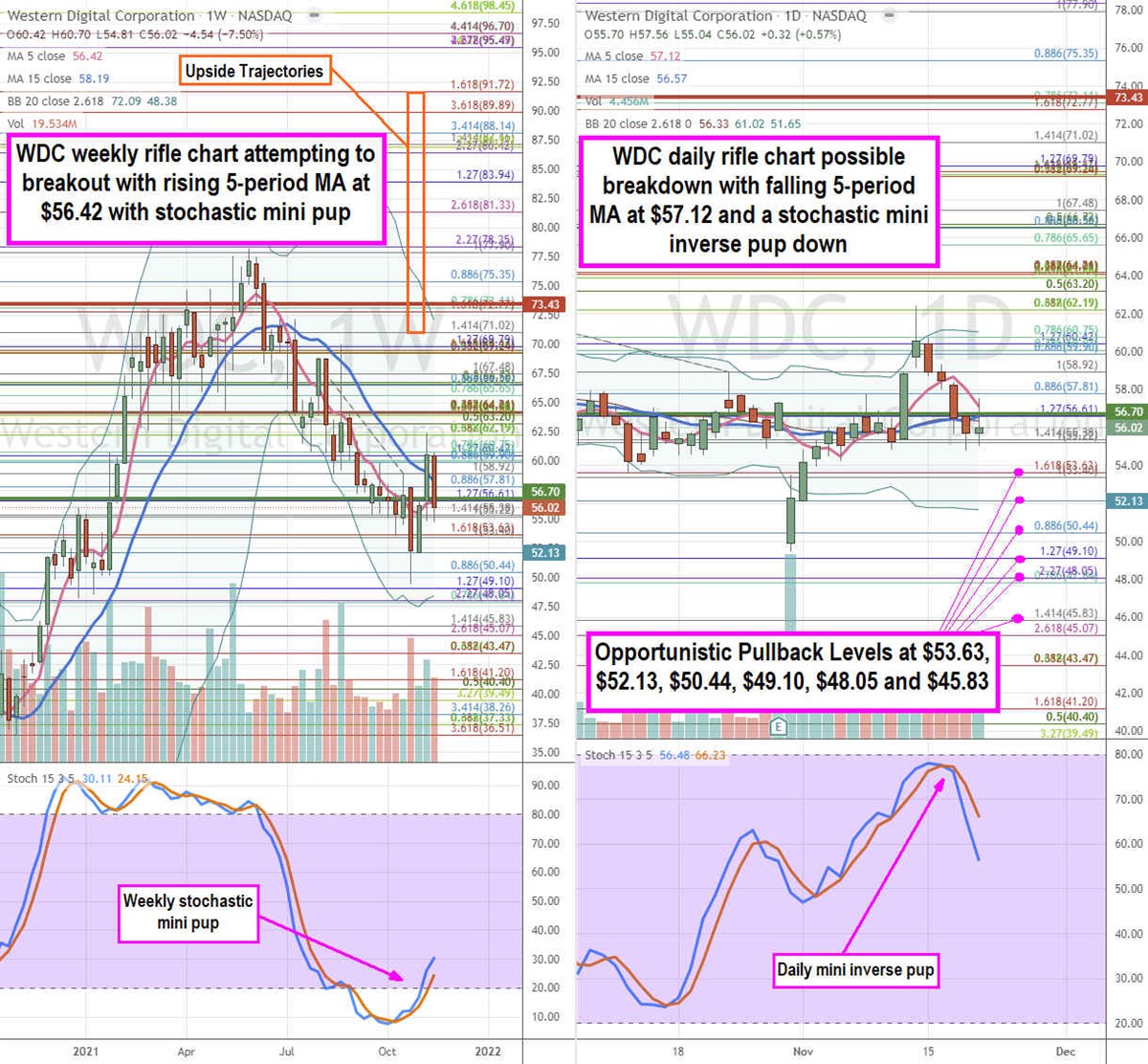

WDC Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provides a precision view of the price action playing field for WDC shares. The weekly rifle chart peaked near the $78.35 Fibonacci (fib) level before plunging to a low of $49.50. The weekly rifle chart coiled on a stochastic mini pup through the 20-band attempting to trigger a weekly market structure low (MSL) buy signal above $56.70. The weekly 5-period moving average (MA) is rising at $56.42 attempting to crossover the 15-period MA at $58.19 for a breakout. The daily rifle chart peaked off the $62.19 fib before slipping on a falling 5-period MA at $57.12 as the daily stochastic mini inverse pup formed. Stochastic is oscillation down through the 40-band with lower daily Bollinger Bands at $51.65.Prudent investors can monitor for opportunistic pullback levels at the $53.63 fib, $52.13 fib, $50.44 fib, $49.10 fib, $48.05 fib, and the $45.83 fib. Upside trajectories range from the $71.02 fib up to the $91.72 fib level.

Market downturns give many investors pause, and for good reason. Wondering how to offset this risk? Enter your email address to learn more about using beta to protect your portfolio.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.