We will unveil the mysteries behind mutual funds, a popular choice among seasoned investors and novices. Join us as we review what to know about mutual funds, providing insights into the mutual fund definition, functionality and the plethora of benefits they offer to individuals looking to grow their wealth.

What is a Mutual Fund?

So, what are mutual funds, and how do mutual funds work? The basic mutual fund definition is a fund serves as an investment vehicle that pools money from numerous small and large investors. These funds are then expertly managed to create a diversified portfolio comprising various assets such as stocks, bonds, cash equivalents and commodities. The primary goal of mutual funds is to spread the mutual fund's risk level out while maximizing its returns by diversifying investments across different securities.

A distinguishing feature of mutual funds lies in their professional management, setting them apart from individual stock investments. Skilled investment professionals, or fund managers, make investment decisions for the fund and its shareholders. These astute managers meticulously analyze market trends, company performance, economic indicators, and other crucial factors to allocate the fund's assets strategically. They aim to seek maximum returns while carefully managing risk.

To begin your understanding of mutual funds, you may ask, "What is a mutual fund vs stock?". While stocks represent ownership in a specific company, mutual funds diversify by investing in various companies across several industries. This diversification plays a vital role in mitigating the impact of any single company's performance on the overall fund. Furthermore, mutual funds allow investors to benefit from the potential gains of multiple companies, even with smaller investment amounts, all while enjoying the advantages of professional management.

Understanding the risk level associated with mutual funds is imperative, just as any investment. Different types of mutual funds carry varying degrees of risk, depending on the assets they hold. For instance, equity-based mutual funds exhibit higher volatility than fixed-income funds. Evaluating your risk tolerance and aligning it with the investment objective and risk profile of the mutual fund you choose is crucial.

Mutual Fund Classes

Mutual fund classes represent different types of shares available within a mutual fund. Investment companies offer these classes and cater to investors' varying needs and preferences. Let's review a list of mutual fund classes and discuss what each class means.

- Class A shares: Class A shares typically involve a front-end sales charge, also known as a "load," which is deducted at the time of purchase. These shares often have lower annual expense ratios compared to other classes. Class A shares may also offer breakpoints, which are volume discounts on sales charges for more significant investments.

- Class B shares: Class B shares typically do not have a front-end sales charge, but they may impose a contingent deferred sales charge (CDSC) if shares are sold within a specified period, usually around five to seven years. Class B shares' annual expense ratios may be higher than Class A shares.

- Class C shares: Class C shares generally do not have a front-end sales charge or a CDSC. However, they may have higher ongoing annual expenses compared to other classes. Like Class B shares, Class C shares may impose a CDSC if sold within a specific period, typically one to two years.

- Class D shares: Class D shares are typically no-load shares that do not impose a front-end or back-end sales charge. They may have higher expense ratios than other share classes and are usually designed for fee-based or fee-only advisors.

- Class F shares: Class F shares are primarily created for institutional investors, such as pension funds and financial advisors. They typically have lower expense ratios and may not have sales charges. Class F shares may require a higher minimum investment amount.

- Class I shares (institutional shares): Class I or institutional shares are designed for institutional investors such as pension funds, endowments or large investment firms. These shares often have lower expense ratios compared to retail share classes. However, they may require higher minimum investments.

- Class R shares (retirement shares): Class R or retirement shares, also known as R-shares, are tailored for retirement accounts like 401(k)s or individual retirement accounts (IRAs). They generally have lower expense ratios and may include features specific to retirement investing, such as simplified withdrawal options or automatic dividend reinvestment.

- Class R6 shares: Class R6 shares are typically designed for retirement plans, such as 401(k)s or other defined contribution plans. These shares often have the lowest expense ratios among share classes and may have no sales charges. The main difference between Class R and Class R6 shares is their fee structures. Class R shares may include sales charges and distribution fees, while Class R6 shares typically have a fee structure that is more straightforward and excludes such charges.

- Class T shares: Class T shares are typically created for retirement plans, such as 403(b)s or other tax-deferred retirement accounts. They may have higher expense ratios than other share classes and often have no front-end sales charge.

- Class W shares: Class W shares primarily target institutional investors or high-net-worth individuals. They usually have lower expense ratios and may require a significant minimum investment.

- Class Y shares: Class Y shares are typically offered to institutional investors, such as pension funds or investment advisors. They generally have lower expense ratios and may have no sales charges.

- Class Z shares: Class Z shares are often designed for institutional investors or high-net-worth individuals. They usually have lower expense ratios and may require a high minimum investment.

It's important to remember that mutual fund classes' availability and specific features can vary among different fund companies. To make informed decisions, investors should carefully review the prospectus and seek guidance from a financial advisor to understand the distinctions between mutual fund classes and select the most suitable option for their investment objectives and circumstances.

Mutual Fund Fees

When investing in mutual funds, it is crucial to comprehend the various fees associated with these investment vehicles. These fees are important to consider as they can impact your overall investment returns. Let's explore the different types of mutual fund fees you may encounter.

- Expense ratio: The expense ratio represents the annual operating expenses of a mutual fund, expressed as a percentage of the fund's average net assets. It covers the costs of fund management, administrative expenses, marketing and other operational expenses. So, what is a good expense ratio for a mutual fund? A reasonable expense ratio for a mutual fund can vary depending on investment strategy, asset class and performance. As a general guideline, lower expense ratios are often preferred as they leave more of the fund's returns in the hands of investors.

- Sales loads: Sales loads are commissions or fees charged when buying or selling shares of certain mutual funds. There are two types of sales loads: front-end loads and back-end loads. Front-end loads, or sales charges, are paid upfront when purchasing fund shares. Back-end loads, also called redemption fees or deferred sales charges, are incurred when selling fund shares within a specific holding period. It's important to note that not all mutual funds charge sales loads, and funds without sales loads are referred to as "no-load" funds.

- Redemption fees: Some mutual funds may impose redemption fees to deter frequent trading or market timing. These fees are typically a small percentage of the amount redeemed and are applied when investors sell their fund shares within a short period after purchasing them. Redemption fees are designed to discourage short-term trading activities that can disrupt the fund's management and negatively impact long-term investors.

- Exchange fees: Exchange fees are applicable when investors transfer their investments from one mutual fund to another within the same fund family. These fees are charged to cover the administrative costs of processing the exchange.

- 12b-1 fees: 12b-1 fees, named after the Securities and Exchange Commission (SEC) rule that allows them, are deducted from a mutual fund's assets to cover distribution and marketing expenses. These fees are included in the fund's expense ratio and can vary among different mutual funds. They are typically charged annually and can range from a fraction of a percentage point to a higher percentage of the fund's net assets.

- Account maintenance fees: Some mutual fund companies may charge account maintenance fees to cover administrative costs associated with maintaining investor accounts. These fees can be assessed annually or quarterly and are separate from the fund's expense ratio.

- Management fees: Management fees represent the compensation paid to the fund's investment advisor or management company for managing the portfolio. These fees are included in the fund's expense ratio and can vary depending on the complexity of the fund's investment strategy and the level of active management involved.

- Custodial fees: In some cases, mutual fund investors may encounter custodial fees charged by the custodian or the institution responsible for holding the fund's assets. These fees cover the costs of safekeeping and administering the fund's securities.

When evaluating mutual fund fees, it's essential to consider the overall cost structure in relation to the fund's investment objective, performance track record and the value it provides to your investment strategy. While a good expense ratio for a mutual fund may vary depending on factors such as the fund's category and investment style, generally, lower expenses can contribute to higher net returns over the long term.

For fixed-income mutual funds, consider fees in the context of the fund's yield and risk profile. Fixed-income funds typically have lower expense ratios than actively managed equity funds due to their more conservative investment approach.

Understanding the various mutual fund fees allows you to make informed decisions and select funds that align with your investment goals and preferences. When comparing mutual funds, consider the complete cost structure, including the expense ratio, sales loads, redemption fees and other associated fees. It's important to note that fees alone should not be the sole determining factor in fund selection. Assess the fund's historical performance, investment strategy, risk profile and the fund management team's expertise.

Types of Mutual Funds

When investing in mutual funds, one size does not fit all. Mutual funds come in various types, each catering to different investment objectives, risk profiles and asset classes. Understanding the various types of mutual funds is essential for investors seeking to build a well-diversified portfolio tailored to their specific needs.

Let's take a few minutes to explore the diverse landscape of mutual funds. By delving into the characteristics and investment strategies of these different types of mutual funds, investors can gain valuable insights into selecting the ones that align with their financial goals and risk tolerance.

Stock Funds

Stock funds, also known as equity funds, primarily invest in stocks or equity securities. They aim to provide long-term capital appreciation by investing in a diversified portfolio of publicly traded companies. Stock funds can focus on specific regions, industries or market capitalizations, such as large-cap, mid-cap, small-cap or blue-chip stocks. They carry varying levels of risk and can categorize further into growth funds, value funds, sector funds, or index funds.

Bond Funds

Bond funds invest in fixed-income securities, such as government, corporate and municipal bonds or mortgage-backed securities. These funds aim to generate income through regular interest payments and potential capital appreciation. Bond funds vary in risk profiles, with some focusing on high-quality investment-grade bonds, while others may include higher-yielding but riskier ones. They can also have different durations, such as short-term, intermediate-term, or long-term bond funds.

Money Market Funds

Money market funds invest in short-term, low-risk instruments, such as Treasury bills, commercial paper, certificates of deposit and short-term corporate debt. These funds aim to preserve capital and provide stability while offering a modest income level. Money market funds are considered relatively safe investments, suitable for investors seeking liquidity and capital preservation.

Index Funds

Index funds aim to replicate the performance of a specific market index, such as the S&P 500 or more focused indexes, such as a fund that tracks the consumer staples index. They invest in a diversified portfolio of securities that mirror the index's composition and weightings. Index funds are passively managed and generally have lower expense ratios than actively managed funds. They offer broad market exposure and are popular among investors seeking a low-cost and efficient way to achieve market returns.

Exchange-Traded Funds (ETFs)

ETFs are similar to index funds but trade on stock exchanges like individual stocks. They are designed to track specific market indexes or sectors. ETFs offer flexibility, allowing investors to buy and sell shares throughout the trading day at market prices. They provide diversification and transparency while offering access to various asset classes, including blue-chip stocks, bonds, commodities and real estate. For income-seeking investors, some ETFs offer dividends.

Balanced Funds

Balanced funds, also known as asset allocation funds, invest in a mix of stocks, bonds and sometimes money market instruments. These funds aim to provide a balanced approach to risk and return, with the allocation between stocks and bonds adjusted based on market conditions and the fund manager's strategy. Balanced funds are suitable for investors looking for a single fund that provides diversification across asset classes.

Income Funds

Income funds focus on generating regular income for investors by investing in dividend-paying stocks, high-yield bonds, preferred stocks or other income-generating securities. These funds aim to provide a steady income stream while maintaining a certain level of capital preservation. Income funds are popular among investors seeking regular cash flow and lower volatility than growth-oriented funds.

International Funds

International funds, also known as global or foreign funds, invest in securities from countries outside the investor's home country. These funds provide exposure to international markets and allow investors to capitalize on global economic growth and diversify their portfolios geographically. International funds can focus on specific regions or offer broad global exposure.

Specialty Funds

Specialty funds target specific investment strategies or sectors, such as real estate, technology, healthcare, or natural resources. These funds concentrate their investments in a particular theme or industry, aiming to capitalize on specialized opportunities. These funds can be closed-end mutual funds or open-end mutual funds. Specialty funds can offer higher growth potential but also carry higher risk due to their focused nature.

These are some of the major types of mutual funds available to investors. Each type offers unique characteristics, risk profiles and investment strategies. It's essential for investors to carefully evaluate their investment objectives and risk tolerance before selecting the appropriate types of mutual funds. Considerations such as investment time horizon, desired level of diversification, income requirements and personal preferences play a crucial role in determining which funds align with individual financial goals.

Why Invest in Mutual Funds?

When building a successful investment portfolio, various options are available to individuals seeking to grow their wealth. One popular and practical choice is investing in mutual funds. Mutual funds have gained significant popularity among investors of all levels due to their unique features and potential benefits. Let's take a few minutes to explore the compelling reasons why many individuals choose to invest in mutual funds. By understanding the reasons behind investing in mutual funds, investors can make informed decisions and evaluate whether mutual funds align with their financial goals, risk tolerance and investment preferences.

- Diversification: Mutual funds allow investors to gain exposure to a wide range of securities, such as stocks, bonds and commodities, which helps spread risk and reduce the impact of any single investment on the overall portfolio.

- Professional management: Mutual funds are managed by experienced investment professionals who conduct research, make investment decisions and monitor the portfolio on behalf of investors. This expertise can be valuable for individuals who may not have the time, knowledge, or resources to manage their investments independently.

- Accessibility: Mutual funds are accessible to investors with various capital levels, offering entry points for small and large investors. Additionally, investors can buy and sell mutual fund shares at the end-of-day net asset value (NAV), making them highly liquid.

- Affordability: Many mutual funds have relatively low minimum investment requirements, allowing investors to start building a diversified portfolio with a modest amount of capital. This affordability makes mutual funds accessible to a broader range of investors.

- Flexibility: Mutual funds offer flexibility in terms of investment strategies and objectives. Funds are available to suit different investment goals, whether long-term growth, income generation, capital preservation or a combination of objectives.

- Convenience: Investing in mutual funds is convenient as it provides a single investment vehicle with a diversified portfolio of securities. This eliminates the need for investors to buy and manage multiple individual securities.

- Transparency: Mutual funds must provide regular reports and disclosures to investors, including prospectuses, annual reports and financial statements. This transparency helps investors understand the fund's holdings, expenses, performance and investment strategies.

- Dividends and capital gains: Many mutual funds distribute dividends and capital gains to their investors. Dividends are typically paid from the income generated by the underlying securities, while capital gains result from the sale of securities within the fund's portfolio. These distributions can give investors regular income or the option to reinvest for potential growth.

- Regulatory oversight: Mutual funds are regulated by governmental bodies, such as the Securities and Exchange Commission (SEC) in the United States. This oversight helps protect investors by ensuring compliance with regulations, promoting fair practices and providing transparency in the mutual fund industry.

- Investor education and support: Mutual fund companies often provide educational resources, tools and customer support to assist investors in making informed decisions. This support can include investment research, online platforms, customer service representatives and access to financial advisors.

By considering these factors and understanding mutual funds' advantages, investors can determine whether they align with their investment goals, risk tolerance and preferences. It's vital for individuals to carefully evaluate these factors and choose mutual funds that suit their specific needs.

Example of a Mutual Fund

When considering an example of a mutual fund, the Vanguard S&P 500 Growth Index Fund NYSEARCA: VOOG stands out for several reasons. One of the main advantages of this fund is its exposure to the S&P 500 Growth Index. By investing in the Vanguard S&P 500 Growth Index Fund, investors can access a diversified portfolio of large-cap U.S. companies expected to have above-average growth potential. This allows them to participate in the potential upside of companies with strong growth prospects.

Another noteworthy advantage of the Vanguard S&P 500 Growth Index Fund is its low costs. Vanguard is known for its low-cost investment approach, and the expense ratio for Vanguard S&P 500 Growth Index Fund is typically lower compared to actively managed funds. This cost efficiency can enhance long-term returns by minimizing the impact of fees on investment performance.

Diversification is a key benefit offered by the Vanguard S&P 500 Growth Index Fund. As an index fund, Vanguard S&P 500 Growth Index Fund invests in a broad range of companies within the S&P 500 Growth Index. This diversification helps reduce the impact of any single company's performance on the overall fund. By spreading risk across multiple sectors and industries, Vanguard S&P 500 Growth Index Fund aims to mitigate volatility and provide a more stable investment option. As an investor familiarizing yourself with the holdings of the Vanguard S&P 500 Growth Index Fund.

Furthermore, the Vanguard S&P 500 Growth Index Fund is passively managed. This means that the fund aims to replicate the performance of the underlying index rather than relying on active investment decisions. This passive management approach contributes to the lower costs associated with the fund.

While the Vanguard S&P 500 Growth Index Fund NYSEARCA: VOOG offers several advantages, it's also important to consider potential disadvantages. One notable limitation is that the fund's performance is tied to the S&P 500 Growth Index. If the companies within the index underperform or the growth outlook changes, the fund's returns may be affected accordingly.

You must monitor your investments to ensure they align with your investment strategy. Reviewing the Vanguard S&P 500 Growth Index Fund's news headlines is one way to stay on top of any fund or strategy changes.

Pros and Cons of Mutual Funds

In the world of investing, mutual funds have gained significant popularity due to their potential benefits and advantages. However, like any investment vehicle, mutual funds also have their drawbacks. In this section, we will explore the pros and cons of mutual funds to help investors understand the potential benefits and limitations of these investment options.

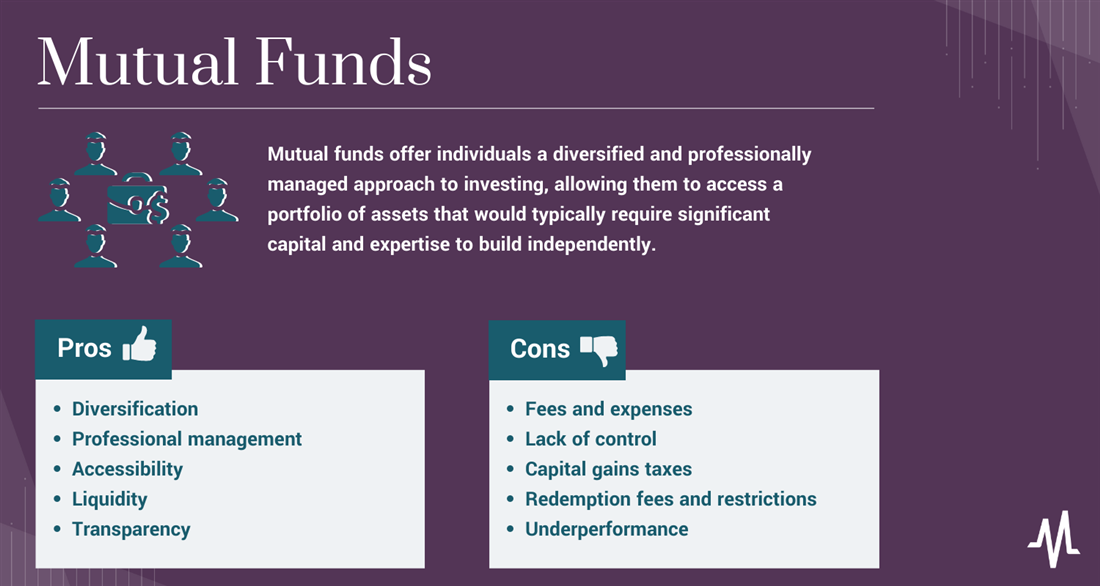

Pros

The pros include:

- Diversification: Mutual funds provide instant diversification by pooling investors' money to invest in various assets, such as stocks, bonds and other securities. This diversification helps mitigate the risk of relying on a single investment and can provide a more stable portfolio.

- Professional management: One of the key advantages of mutual funds is the access to professional fund managers who make investment decisions on behalf of the investors. These experienced professionals analyze market trends, conduct research and actively manage the fund's portfolio to seek potential opportunities and maximize returns.

- Accessibility: Mutual funds offer a low barrier to entry, making them accessible to a wide range of investors. Individuals with smaller investment amounts can gain exposure to a diversified portfolio that would otherwise require significant capital and expertise to build independently.

- Liquidity: Mutual funds are generally considered liquid investments, meaning investors can buy or sell shares on any business day at the fund's net asset value (NAV). This liquidity allows investors to access their money relatively quickly compared to other investment options.

- Transparency: Mutual funds are required to disclose their holdings, expenses, performance and other important information regularly. This transparency provides investors with the necessary data to make informed investment decisions and evaluate the fund's performance.

Cons

The downsides include:

- Fees and expenses: Mutual funds charge various fees, including management fees, administrative expenses and sales loads. These costs can eat into the investment returns over time and you should carefully consider them before investing. Additionally, actively managed funds often have higher expense ratios than passively managed index funds.

- Lack of control: When investing in a mutual fund, investors surrender some control over the investment decisions to the fund manager. While this can be advantageous in professional management, it also means that investors cannot customize their portfolio according to their specific preferences or investment strategies.

- Capital gains taxes: Mutual funds distribute capital gains to their shareholders, which can result in taxable events for investors, even if they did not sell their shares. This tax liability can impact the overall returns and should be considered, especially for taxable accounts.

- Redemption fees and restrictions: Some mutual funds impose redemption fees or have restrictions on frequent trading to discourage short-term speculation. These fees and restrictions can limit investors' flexibility, especially if you need to access your money quickly or frequently change your investment strategy.

- Underperformance: While many mutual funds aim to outperform their benchmark or peers, not all funds are successful in achieving this objective. Investors run the risk of selecting funds that underperform their benchmarks or fail to meet their investment objectives, resulting in lower returns than expected.

It's important to note that the pros and cons of mutual funds can vary depending on the specific fund, investment strategy and individual investor preferences. Therefore, investors should carefully evaluate these factors and consider their investment goals, risk tolerance and time horizon before investing in mutual funds.

How to Choose the Right Mutual Fund Mix

Choosing the right mutual fund mix is crucial in building a well-diversified investment portfolio that aligns with your financial goals and risk tolerance. Let's review a step-by-step explanation of choosing the right mutual fund mix for you.

Step 1: Determine your investment goals.

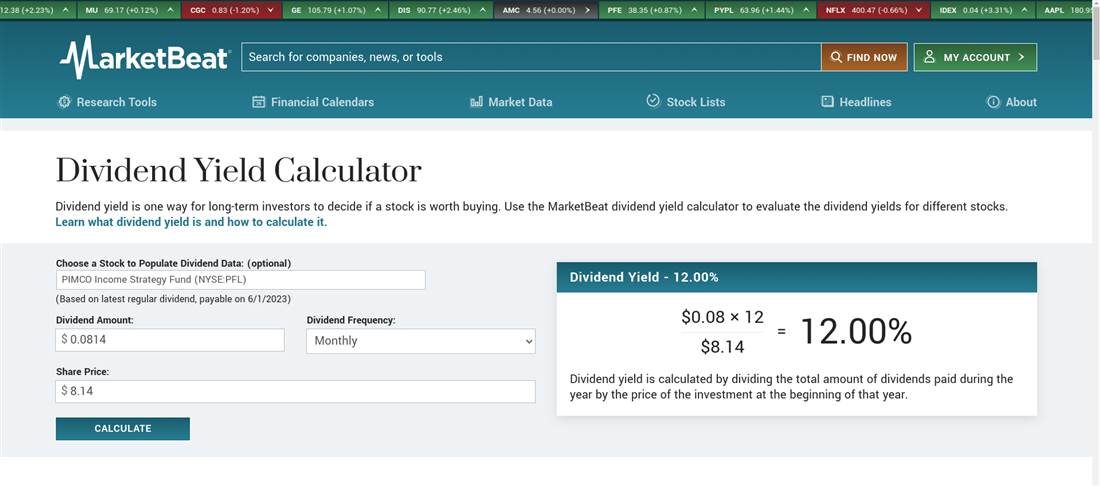

Begin by defining your investment objectives. Are you investing for long-term growth, income or a specific financial milestone? For instance, if you invest for income, you will want to decide what dividend yield works best for you. Clarifying your goals will help guide your selection process. To help you clarify these goals, MarketBeat provides a dividend yield calculator, which helps you determine the yield for different stocks.

Step 2: Assess your risk tolerance.

Evaluate your risk tolerance, considering factors such as your age, time horizon, financial obligations and comfort level with market fluctuations. Determine whether you are conservative, moderate, or aggressive regarding risk.

Step 3: Understand your time horizon.

Consider your investment time horizon, which is the length of time you plan to hold your investments before needing the funds. Longer time horizons may allow for more aggressive investment strategies, while shorter ones may require a more conservative approach.

Step 4: Research different fund categories.

Explore the various mutual fund categories available, such as equity, bond, money market and specialty funds. Each category has different risk and return characteristics, so understanding their features is essential.

Step 5: Evaluate fund objectives.

Within each fund category, analyze the specific objectives of the funds. For example, growth, value or sector-specific funds may be within equity funds. Assess whether the fund objectives align with your investment goals.

Examine the historical performance of the funds you are considering. Look for consistent returns over a reasonable period and compare the fund's performance to its benchmark index or peer group.

Step 7: Consider fund expenses.

Evaluate the expense ratios and fees associated with each fund. Lower expense ratios can positively impact your investment returns over time, so compare fees across similar funds.

Step 8: Assess fund management.

Research the fund managers' track record and experience. Look for managers with a strong investment philosophy, consistent performance and a disciplined approach to portfolio management.

Step 9: Analyze fund holdings.

Review the fund's holdings to gain insights into asset allocation and diversification. Ensure the fund's holdings align with your desired diversification and risk exposure level.

Step 10: Consider fund size and liquidity.

Evaluate the fund's size and liquidity. While larger funds may offer stability and resources, smaller funds may have the potential for greater agility and flexibility. Consider your preference for fund size based on your investment needs.

Step 11: Read the fund prospectus and reports.

Read the fund's prospectus and reports, which provide detailed information about the fund's investment strategy, risks, expenses and performance. This information will help you make an informed decision.

Step 12: Compare funds to each other.

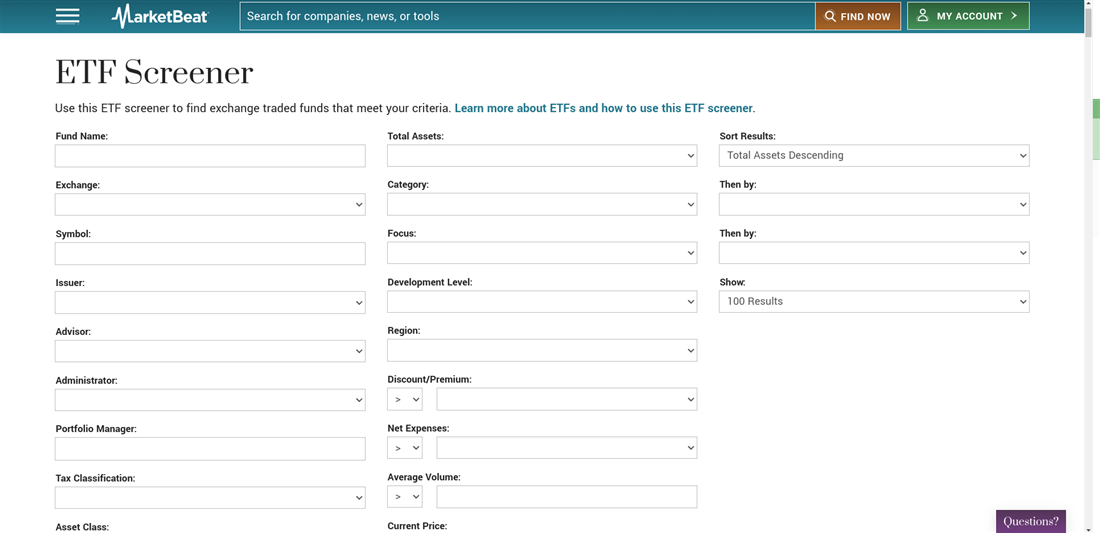

Once you have conducted thorough research and narrowed down your selection of potential mutual funds, it is essential to compare them. This comparative analysis will help you decide and find the fund that best suits your investment goals. Start by reviewing the fund's investment objectives and determining if they align with your objectives. Evaluate the historical performance of the funds over different periods and compare them to their benchmark index or similar funds. Assess each fund's risk and volatility and consider your risk tolerance. Additionally, analyze the funds' expense ratios and choose ones with competitive fees. Use tools such as MarketBeat's ETF Screener to research the funds further. Comparing funds to each other will provide valuable insights to guide your final decision.

Step 13: Monitor and review your portfolio.

After selecting a mutual fund mix, regularly monitor and review your portfolio's performance. Periodically reassess your investment goals, risk tolerance and market conditions to ensure your mutual fund mix remains suitable for your needs.

Remember, selecting the right mutual fund mix is a dynamic process that may require adjustments over time. As your circumstances change and market conditions evolve, you must periodically review and rebalance your portfolio to maintain a suitable asset allocation and achieve your investment objectives.

Build Wealth with Mutual Funds

In conclusion, mutual funds have transformed the world of investing by offering individuals a convenient and diversified approach to growing their wealth. By delving into the core concepts of mutual funds, including their definition, workings and types, investors can confidently navigate this realm and make informed decisions that align with their financial goals.

As you embark on your investment journey, it is crucial to consider key factors when selecting mutual funds. Consider your investment objectives, risk tolerance, expense ratios and past performance. By carefully evaluating these aspects and diversifying your portfolio across different funds, you can position yourself for long-term success and potentially achieve your financial aspirations.

Mutual funds provide a powerful combination of professional management, diversification and accessibility. Whether you are an experienced investor or just starting out, mutual funds offer the opportunity to participate in the growth of various asset classes and companies. It is important to conduct thorough research, understand each fund's pros and cons, and choose a well-balanced mix that aligns with your investment objectives.

By exercising patience, diligence and implementing a sound investment strategy, mutual funds can become a valuable tool on your journey to financial prosperity. Embrace the potential they offer, stay informed and remain committed to your long-term goals. With mutual funds as part of your investment portfolio, you can navigate the ever-changing financial landscape and pave the way for a brighter financial future.

FAQs

As we conclude our exploration of mutual funds, let's address some frequently asked questions that may still be lingering in your mind. Let's review some of the answers to these questions to help deepen your understanding of mutual funds.

What is a mutual fund?

A mutual fund is an investment vehicle that pools money from multiple investors to create a diversified portfolio of securities such as stocks, bonds and other assets. Skilled fund managers professionally manage them and make investment decisions on behalf of the investors.

How do you make money on mutual funds?

Two primary ways to make money with mutual funds include capital appreciation and dividends. When the value of the fund's holdings increases, the share price rises, resulting in capital gains when you sell your shares. Additionally, some mutual funds distribute dividends or interest income earned from the fund's investments to the shareholders.

What's the difference between a mutual fund and ETF?

While mutual funds and exchange-traded funds (ETFs) are investment vehicles that pool money from multiple investors, there are notable differences. Mutual funds are priced once a day at the end of the trading day, and their prices are determined by the fund's net asset value (NAV). On the other hand, ETFs trade on an exchange like stocks throughout the day, and their prices fluctuate based on supply and demand. Additionally, ETFs often aim to replicate the performance of a specific index, while mutual funds may have different investment strategies.