NVIDIA NASDAQ: NVDA is the most important stock in the market but not the only one benefiting from AI or its advances. Peripheral businesses like Micron Technology NASDAQ: MU and collaborators like Logitech International NASDAQ: LOGI and Uber Technologies NYSE: UBER are well-positioned. They are positioned to benefit from demand in the first case and advancement of AI in the other, and more importantly, able to capitalize on it.

Why Micron’s HBM3E Technology Leads the Industry

Micron Technology Today

MU

Micron Technology

$99.57 +0.16 (+0.16%) As of 11:34 AM Eastern

- 52-Week Range

- $79.15

▼

$157.54 - Dividend Yield

- 0.46%

- P/E Ratio

- 146.43

- Price Target

- $135.24

Micron’s HBM3E technology is the best and would be in high demand with or without NVIDIA. HBM3E provides the capacity to run the most advanced cloud applications with better performance and lower power usage than its competitors. It just so happens that NVIDIA’s GPUs and CPUs are central to the rise in AI and driving the demand today. That and normalization in legacy markets have Micron’s revenue growing at a hyper pace in 2025 and forecasted to remain robust in the subsequent year. Among the critical details is the margin, which is widening due to strength in the higher-margin next-gen end-markets and revenue leverage.

The consensus estimates for 2025 and 2026 rose at the end of 2024 but are likely low due to the demand and ramping capacity. The company is expanding its HBM footprint with a $7 billion facility expected to commence operations in early 2026, and other links in the AI supply chain are doing likewise. Taiwan Semiconductor is ramping capacity in several locations, increasing its capacity outlook while paving a path to onshoring production of NVIDIA’s most advanced technology. Regarding the price targets, analysts' consensus reported by MarketBeat forecasts this stock to trade near $135 or 35% upside from early January trading levels.

Uber and NVIDIA Aim to Disrupt the Autonomous Vehicle Industry

Uber Technologies Today

UBER

Uber Technologies

$66.16 +1.25 (+1.93%) As of 11:34 AM Eastern

- 52-Week Range

- $54.84

▼

$87.00 - P/E Ratio

- 32.92

- Price Target

- $91.53

Uber and NVIDIA are collaborating on a program harnessing Uber’s data generation capability and NVIDIA’s AI computing power to advance autonomous driving. While still a future event, the move to autonomous driving will open new revenue opportunities for this company, allowing it to evolve with technology, and the outlook is bright.

The analysts forecast double-digit growth for Uber over the next few years, with improved earnings quality. The company has already significantly improved its earnings quality, as seen in the 2024 report, and begun aggressive capital returns because of it. Capital returns are expected to continue and possibly strengthen, providing market support at crucial times through buybacks while improving shareholder value.

Analysts like Uber. Not only is coverage rising, but sentiment is firm at Moderate Buy, and the price target is trending higher. The activity is mixed; there were some downgrades and price target reductions in 2024, but the positive outweighs the bad, leaving the consensus target up nearly 60% for the year and 40% above the early January price action.

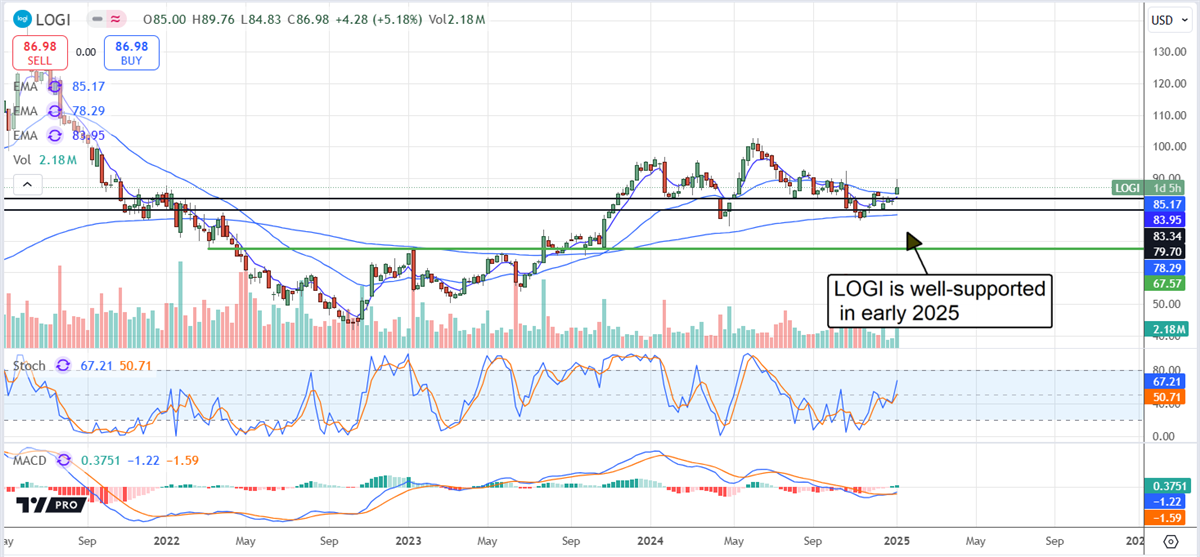

Logitech Advances Streaming Capability: NVIDIA Expands AI Use-Cases

Logitech International Today

LOGI

Logitech International

$85.42 -1.56 (-1.79%) As of 11:34 AM Eastern

- 52-Week Range

- $74.72

▼

$102.59 - Dividend Yield

- 0.61%

- P/E Ratio

- 19.02

- Price Target

- $92.88

Logitech, NVIDIA, and Inworld AI collaborated on an AI agent for streamers. The tool on G’s Streamworld provides a 3-D assistant that can co-host while automating production. While having a small impact on revenue, the assistant is yet another feature that sets Logitech apart from competitors. Logitech is the leading manufacturer of peripheral devices for computers and services to support them; integrating AI agents into its ecosystem is a natural progression.

Regarding Logitech’s revenue and earnings outlook, the company is expected to sustain growth in 2025 and accelerate it over the next few years. Earnings are forecasted to grow more than 50% by 2030, putting this stock at a 14x valuation and deep-value territory.

Logitech’s dividend is part of its appeal. The stock isn’t a high-yield, but it is competitive, with the S&P 500 running near 1.5% and reliable. The company pays only 25% of its current year earnings outlook and has a solid record of increases. The company has increased its payment at a double-digit CAGR for over a decade and should sustain long-term growth at this pace due to balance sheet health, improving cash flow, and the earnings growth outlook.

Before you consider Micron Technology, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Micron Technology wasn't on the list.

While Micron Technology currently has a "Moderate Buy" rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Click the link below and we'll send you MarketBeat's guide to investing in 5G and which 5G stocks show the most promise.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.