Defense stocks are pulling back following Q1 reports from Lockheed Martin NYSE: LMT, Northrop Grumman NYSE: NOC, and RTX NYSE: RTX. The primary cause is uncertainty, followed by tepid guidance. Regarding uncertainty, companies face an unknown impact from tariffs that could affect their profitability. That is a risk that can’t be ignored.

Each company reaffirmed its 2025 outlook, calling for growth and enough cash flow to maintain financial strength, reinvest in operations, and return capital to shareholders.

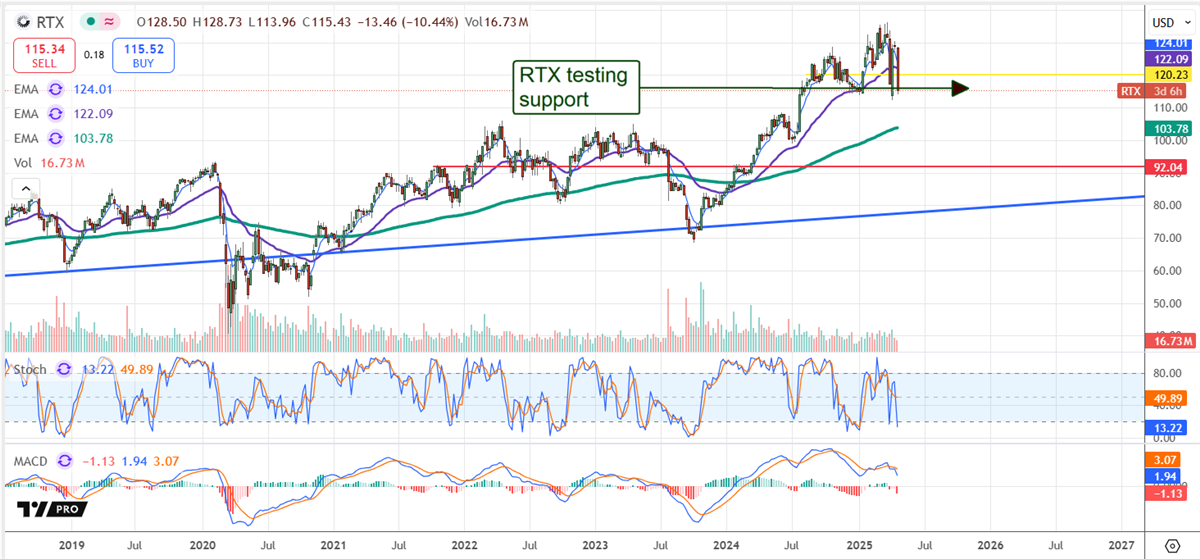

RTX: Solid Results With Long-Term Upside

RTX Today

$124.36 +2.39 (+1.96%) As of 12:14 PM Eastern

This is a fair market value price provided by Polygon.io. Learn more. - 52-Week Range

- $99.07

▼

$136.17 - Dividend Yield

- 2.03%

- P/E Ratio

- 35.03

- Price Target

- $161.38

RTX is the standout in Q1. It outperformed on the top and bottom lines, with earnings growth of 10%, driven by strength in key segments like drones and unmanned equipment. Margin news is also good, and guidance was reaffirmed.

Its repurchases did not offset the dilutive actions in Q1, but they do over time. Capital returns remain a core part of the story.

Backlog continues to grow, with new contract wins adding to the already strong pipeline. Analysts see the most upside here, with MarketBeat’s consensus target forecasting up to 40% gains. However, upside will likely be limited in 2025 until there is more clarity in the tariff outlook.

Lockheed Martin: Consistent Execution

Lockheed Martin Today

LMT

Lockheed Martin

$473.59 +6.78 (+1.45%) As of 12:14 PM Eastern

This is a fair market value price provided by Polygon.io. Learn more. - 52-Week Range

- $418.88

▼

$618.95 - Dividend Yield

- 2.79%

- P/E Ratio

- 21.28

- Price Target

- $544.79

Lockheed outperformed on revenue and earnings in Q1, with earnings growth of roughly 15%. The strength was broad, but especially strong in unmanned systems. Space remains a weak spot, but not enough to derail the story.

Lockheed’s capital returns were substantial. Buybacks reduced the share count by 2.6% for the quarter, and the dividend yield sits at 2.9%, the highest of the group. The payout is well-covered and expected to grow.

The backlog is healthy, adding to the sector’s collective $485 billion in orders—about 10 quarters' worth of revenue at the current pace. Volatility is low, and institutional interest remains high heading into Q2.

Northrop Grumman: Weakness Priced In?

Northrop Grumman Today

NOC

Northrop Grumman

$464.36 +1.29 (+0.28%) As of 12:14 PM Eastern

This is a fair market value price provided by Polygon.io. Learn more. - 52-Week Range

- $418.60

▼

$555.57 - Dividend Yield

- 1.77%

- P/E Ratio

- 16.38

- Price Target

- $542.94

Northrop’s Q1 miss was tied to the expected wind-down of Space-related operations and increased costs in the B-21 program. Even so, the company reaffirmed its guidance, forecasting annual growth with expansion in all segments, including Space.

Buybacks were more substantial than peers, reducing the share count by 3% for the quarter. The dividend yield is the lowest at 1.5%, but also the safest, with a payout ratio near 35%. Capital returns are well-supported and expected to grow.

Margins were impacted by one-offs but were not enough to alter the company’s financial health. Consulting signings increased, and the book-to-bill ratio remains strong.

Sector Snapshot: Under Pressure But Holding Up

Defense stocks had a solid Q1 overall, despite some spotty weaknesses and the impact of divestitures. A key detail is that diversified business models—balancing private and public contracts—are sustaining operations. All reported strength in critical segments, including drones and unmanned equipment, with Space a noteworthy weakness across the board.

Backlog is a critical factor. Each reported contract wins and backlog growth, including record levels for some. The takeaway is that the collective, roughly $485 billion backlog equates to 10 quarters of revenue at the Q1 pace, providing ample visibility.

Analyst and Institutional Trends Remain Positive

The analysts' trends support defense stock markets in 2025, including increasing coverage, steady or firming sentiment, and steady or firming consensus price targets. The consensus price targets reported by MarketBeat forecast minimum double-digit upsides for these stocks, ranging from 20% to 40%.

Likewise, the institutional trends also support defense stocks in 2025. Those trends include high levels of ownership compounded by multi-year high activity in Q1 and buying persisting in Q2. Assuming these trends continue, these stocks are unlikely to fall significantly further in Q2 and could begin to rebound before the start of the second half.

Among the catalysts is a promise from Trump to boost defense spending in 2026 by as much as 12% to ensure America’s unmatched military strength. Additionally, the President continues to push for increased spending by NATO nations.

Volatility, or lack of it, is yet another reason defense stocks are good buys in 2025. These stocks trade at a significantly lower beta than the S&P 500, providing some insulation from day-to-day market movements and sharp, broad market declines.

Before you consider Northrop Grumman, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Northrop Grumman wasn't on the list.

While Northrop Grumman currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

If a company's CEO, COO, and CFO were all selling shares of their stock, would you want to know? MarketBeat just compiled its list of the twelve stocks that corporate insiders are abandoning. Complete the form below to see which companies made the list.

Get This Free Report