AI is a powerful tool helping many SaaS companies today. The bad news (at least for some) is that AI will drive a shakeout in the industry and change its face forever. The problem is that the tools and power AI provides to the SaaS vendors are also provided to businesses savvy enough to use them. That is already happening as many companies begin to move in-house what were once sought-after services.

The meaning? Enterprises with the size, scale, and resources will cut ties with SaaS vendors, leaving them to fight over the smaller businesses that still need their technology.

Klarna is a leading example. Klarna is a Sweden-based fintech specializing in payments, buy-now-pay-later, and other consumer financing needs. It has been working diligently to lower its costs and is using AI. Earlier this year, it announced a 25% savings in marketing agency spending driven by AI, which it compounded recently when it announced cutting ties with Salesforce NYSE: CRM and Workday NASDAQ: WDAY. Salesforce and Workday are leading SaaS providers that serve customer engagement and workflow automation needs.

Klarna CEO Sebastian Siemiatkowski says the company is shutting down many SaaS vendors because of internal efforts to simplify. It’s been using AI to standardize workflows and create a lighter-weight tech stack, enabling workforce reductions and other efficiencies. AI already does the work of 700 employees and has reduced outcome times by 82% to two minutes from eleven, significantly boosting revenue quality. Revenue per employee is up nearly 75% and is increasing earnings leverage. Klarna says it targets another nearly 50% reduction in the workforce but did not put a timeline on it.

Salesforce Grows, Growth Slows, Valuation Comes Into Play

Salesforce Today

$281.56 +2.53 (+0.91%) As of 03/21/2025 03:59 PM Eastern

This is a fair market value price provided by Polygon.io. Learn more. - 52-Week Range

- $212.00

▼

$369.00 - Dividend Yield

- 0.57%

- P/E Ratio

- 46.31

- Price Target

- $362.74

Salesforce is still growing and will likely outperform its consensus estimates for the 2nd half because its services drive results and resonate with businesses that are too small or unwilling to do AI alone. The problem with its share price is that growth is slowing due to its large size, which is a headwind for the market. With acceleration out of the picture and the days of double-digit growth a thing of the past, a premium valuation is no longer warranted, which is reflected in the price action.

The analysts are optimistic that growth can be sustained at a high-single-digit pace through year’s end and into 2025. More than 65% of the revisions since the last earnings release are higher and have significantly lifted the consensus revenue figure. However, the analysts may still underestimate growth due to client acquisition and penetration trends. Salesforce tends to outperform nearly 100% of the time.

The analysts are also optimistic that the stock price can increase by 20% over the next twelve months, but caution has entered the picture. The latest update is from Oppenheimer, which cautioned about software companies generally, citing weakening technical trends that may keep their markets under pressure for the remainder of the calendar year 2024.

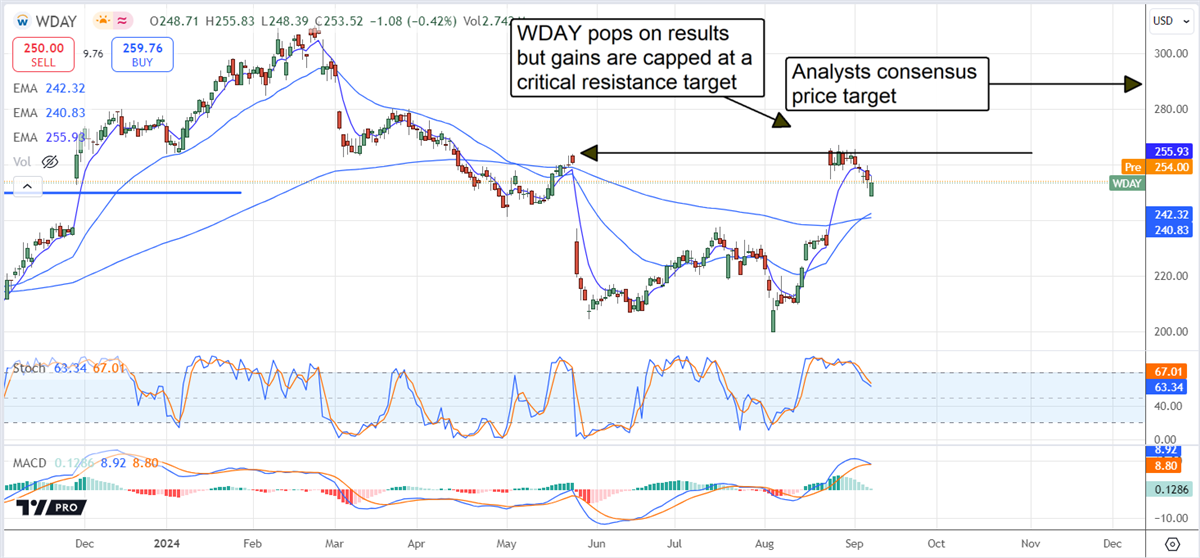

Workday Sustains Double-Digit Growth

Workday is a smaller but no less critical part of the AI-driven SaaS revolution. This company's revenue growth is in the mid-teens in 2024 and is expected to sustain that pace in 2025. Its growth is driven by its ease of use, plug-and-play platform modules, and scalable automation tools. It is perfect for smaller businesses looking to maximize their growth and earnings.

Workday Today

$249.49 -0.98 (-0.39%) As of 03/21/2025 04:00 PM Eastern

- 52-Week Range

- $199.81

▼

$294.00 - P/E Ratio

- 41.37

- Price Target

- $300.36

Highlights from its Q2 results include top-and-botom-line strength and better-than-expected guidance aided by a new deal with Equifax. Workday will help Equifax automate its verification process, speeding up operations and improving consumer outcomes. Workday also announced a new collaboration with Salesforce that will aid revenue growth for both. Other highlights from Q2 include improved cash flow, dilution reducing share repurchases, and improved shareholder equity.

The analyst response to Workday’s Q2 results and full-year outlook was overwhelmingly bullish, leading the market to the high end of the target stock price range. More than 90% of the revisions included an increased price target, increasing the consensus target, which assumes a 15% upside for the stock. A move to consensus aligns the market with the recent highs and the top of a trading range that could cap gains if growth begins to slow.

Before you consider Workday, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Workday wasn't on the list.

While Workday currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

MarketBeat just released its list of 10 cheap stocks that have been overlooked by the market and may be seriously undervalued. Enter your email address and below to see which companies made the list.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.